Mizuho was proud to sponsor the 2023 Annual Private Placement Conference in Miami, Florida this January. The conference allowed issuers and investors across all sectors and geographies the chance to review major trends of 2022 while planning for the current year. The Mizuho Private Placement team hosted several issuer clients as well as met with many global investors over the course of the three days. Managing Director, Sameer Kishore participated on a panel with other leading banks in the market to discuss industry trends and the outlook for private placements in 2023.

The Main Takeaway

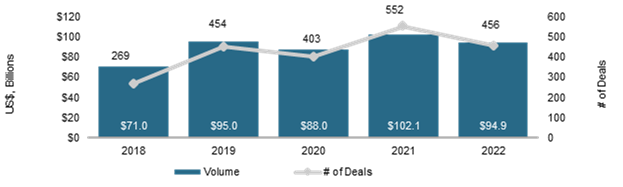

Despite global volatility, macro uncertainty and recessionary fears, the market remains open and is growing both new issuers and investors. While annual issuance volume was down modestly from a record 2021 (~$95 billion in 2022 vs ~$100 billion in 2021), the market did not shut down throughout the year. Consensus from market participants is that 2023 will be a strong year. Looking back, issuance volume has grown over 230% since the depths of the Global Financial Crisis to today. Moreover, even as global public markets waned, we continued to see diversified investors entering the market providing new sources of capital, negotiated terms and the ability to fund larger transactions than ever before.

Annual New Issuance Volume

Source: Private Placement Monitor and Refinitiv as of December 31, 2022

The Supply Dynamic: New Names, Bigger Deals

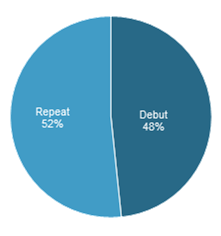

Debut issuances were a key driver of market supply with nearly half of all deals in 2022 (48%) coming from new names to the private market. Conversations with new issuers at the conference revealed their desire for investor diversification, execution certainty and more customized financing solutions as some of the main reasons global issuers chose to tap the private market for the first time. Repeat issuers cited greater depth of demand from investors, the ability to fund multiple currencies, confidentiality, and longstanding relationships with a large investor base as drivers to return to the market. In 2022, average deal size was $208 million driven by many utility operating companies. However, 25 deals over the past two years have crossed the $1 billion threshold including five in 2022 and three already in January 2023, proving the market has appetite for large deals. (We would be remiss if we were to not mention Mizuho was a lead agent on 2 of these 3 jumbo deals last month). Of note, several issuers have in excess of $5-6 billion outstanding in the market and in some instances issuers are private and unrated. This is a far cry from the market from 8-10 years ago when many issuers were forced to migrate to other markets because of lack of investor demand at much lower thresholds.

Profile of Issuers in 2022

Source: Private Placement Monitor and Refinitiv as of December 31, 2022

Global Expansion

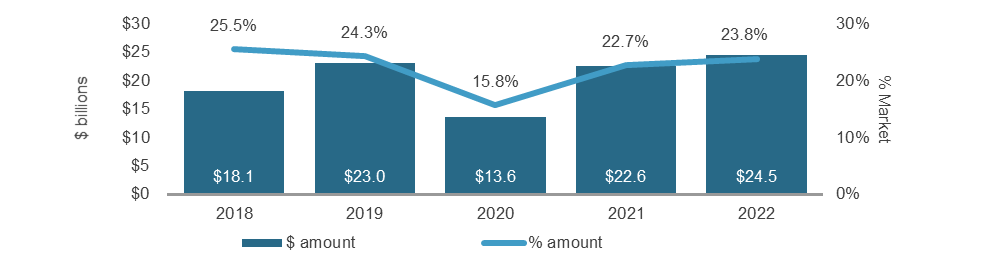

With the War in Ukraine, trade sanctions and a more restrictive worldwide landscape, global issuance accounted for 40% of deal flow in 2022 vs 36% in 2021, with offshore issuers continuing to be a stalwart of the market. Disruptions in supply chain logistics, energy and the shift to a more regional policy by some governments are leading factors for global issuers to seek long-term capital from investors.

Geographically, North America, Western Europe and Australia have traditionally accounted for ~95% of the market in recent years; but an uptick in issuers from Latin America and Asia show these participants are increasingly focused on this market and asset class. Of note, Mizuho led a transaction in 2022 for the first private placement completed by a Japanese issuer. Furthermore, in 2022, several US-based Investment Grade issuers tapped the private market for access to foreign currency such as Japanese Yen as pricing and terms were more competitive in the private market than local or public bond markets at the time.

Non-USD Private Placement Issuance Volume

Source: Private Placement Monitor and Refinitiv as of December 31, 2022

More Money at Play: New Investors Enter the Scene

A record amount of investors participated in the transactions in 2022. Historically 60-70 institutions had been involved in the market with 30-40 possessing dedicated groups focused on the asset class. Over the past few years, the overall number has grown to over 100 institutions with large asset managers, alternative credit funds and third party managed accounts looking to deploy funds in the market. In the search for yield, duration and diversification, more investors have found value in private placements as they look to supplement their investments in more traditional public markets. After years of the buyer base being comprised solely of US life insurance companies, the likes of Blackrock, Blackstone, KKR, Ares, GSAM, Carlyle and Neuberger Berman have set up dedicated teams to help manage investments on behalf of their clients as well as their own money. The result has been a positive for issuers especially in 2022 as the need for new capital and funding certainty became a priority for issuers in light of the increase in interest rates and global equity volatility.

2023 and Beyond

While plenty of challenges lay ahead including the increase in overall funding costs and the near term outlook for interest rates unlikely to revert to pre-pandemic levels for issuers, the fundamentals of the market remain strong. The expansion of private credit as an asset class will continue to grow providing advisors, sponsors, issuers and investors the ability to have more meaningful conversations with respect to a fulsome suite of financing solutions and terms.

We invite you to meet with our dedicated professionals to discuss financing alternatives in the private placement markets.