1. Mizuho Securities USA LLC ("MSUSA")

2. Mizuho Capital Markets LLC ("MCM")

3. Mizuho Bank (USA) (“BKUSA”)

4. Mizuho Bank, Ltd. (“MB”)

5. Mizuho Securities Canada Inc. (“MSCN”)

6. Mizuho Markets Americas (“MMA”)

7. Greenhill Regulatory Disclosures (For All Entities)

8. Anti-Money Laundering Disclosures

9. Sharing of Corporate Customer Information to Group Companies

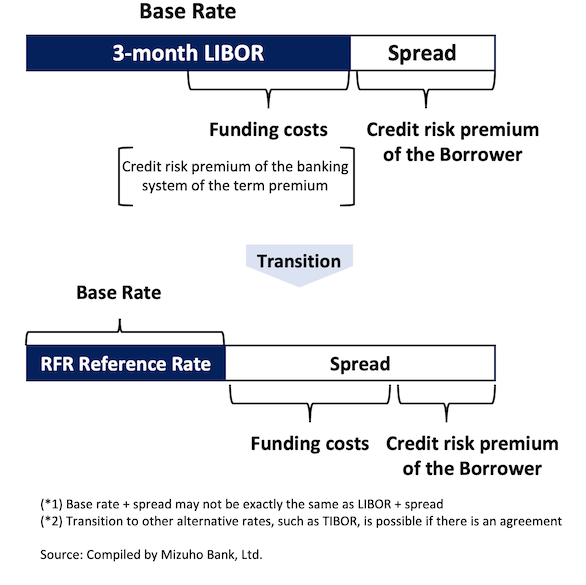

10. Benchmark Rate Reform and Transition to Risk Free Rates

11. Mizuho Americas Pre-Hedging Disclosure

12. Health Care Price Transparency Disclosures

13. Voluntary Carbon Market Disclosure Act (AB1305) Compliance Statement

14. Notice to Commercial Customers Concerning Transactions Related to Unlawful Internet Gambling

15. Economic Sanctions Disclosure

1. Mizuho Securities USA LLC (“MSUSA”)

a. General Disclosures and Disclaimers

Read about the Mizuho Securities USA LLC conversion as of April 1, 2017.

Investment information contained on the Mizuho website is for informational purposes only and does not constitute a recommendation, offer, general solicitation or confirmation of terms. Certain investments and investment strategies mentioned on the website may not be suitable for you. You should weigh any investment decision carefully after considering your specific investment objectives and financial circumstances.

Investment information contained in the website is based upon generally available information believed to be reliable, but no representation is made as to the accuracy, timeliness or completeness of such information or that any returns indicated will be achieved. Changes to assumptions may have a material impact on returns. Price/availability is subject to change without notice. Past performance is not indicative of future results. MSUSA and its affiliates may have accumulated a long or short position in any subject investment.

The investment information contained on the website is not intended for distribution or use in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. Representatives of MSUSA may only conduct business in jurisdictions where they are licensed or exempt from licensing requirements. Clients should contact a MSUSA representative in their home jurisdiction unless governing law permits otherwise. MSUSA is primarily regulated in the US by the Securities and Exchange Commission (“SEC”), the Financial Industry Regulatory Authority (“FINRA”), the Commodity Futures Trading Commission (“CFTC”), the National Futures Association (“NFA”), the Municipal Securities Rule Board (“MSRB”) and CME Group, Inc., and is a member of most major futures exchanges.

FINRA Rule 2266 SIPC Information

MSUSA is a member of SIPC. Clients may obtain information about SIPC, including the SIPC brochure, by contacting SIPC at www.sipc.org or by calling 202-371-8300.

FINRA Rule 2267 Investor Education and Protection

BrokerCheck is a free tool that provides investors with the ability to research backgrounds, experience and conduct of financial brokers, advisors and firms. Investors seeking this information can call the BrokerCheck help line at (800) 289-9999 or visit the BrokerCheck website at http://brokercheck.finra.org. An investor can obtain a brochure containing information on the BrokerCheck program from the help line or website.

b. Research Disclosures

Compensation of Research Analysts

The research analysts principally responsible for MSUSA research reports do not receive any compensation that is directly or indirectly related to the specific recommendations or views expressed by that research analyst. The research analysts may receive compensation based upon various factors, including quality of research, investor client feedback, stock picking, competitive factors, firm revenues and overall investment banking revenues.

Research Reports Prepared by Foreign Affiliates

MSUSA may distribute research reports prepared by its foreign affiliates. Persons wishing to effect transactions in securities discussed in such reports should contact MSUSA. Research reports prepared by our foreign affiliates will be authored by analysts employed by the foreign affiliate. Such persons are not registered with FINRA or associated persons of MSUSA. Employees of our foreign affiliates are subject to their local regulations and not subject to the restrictions set forth in FINRA Rules 2241 and 2242 on communications with a subject company, public appearances and trading securities held by a research analyst account.

c. Order Handling and Trading Disclosures

Investors Exchange LLC (“IEX Exchange”)

As MSUSA is a member of the IEX exchange, customers will be provided copies of the IEX Rulebook upon request or may find a copy of the IEX Rulebook by using the electronic link attached below.

https://cdn.prod.website-files.com/635ad1b3d188c10deb1ebcba/68d2f5a0843e7ee527adabcd_Investors%20Exchange%20Rule%20Book%2009-23-25.pdf

Cboe BYX Exchange Inc. and Cboe BZX Exchange Inc. (“BYX” and “BZX”)

As MSUSA is a member of both the BYX and BZX exchanges, customers will be provided copies of the BYX and BZX Rulebooks upon request or may find a copy of the BYX and BZX Rulebooks by using the electronic links attached below.

If you are considering a trading relationship with Mizuho Securities USA LLC (“MSUSA”), MSUSA is a self-clearing broker-dealer (as defined by the FINRA) for Japanese and US equity products, and has contracted for local Japanese clearing and settlement services with Mizuho Securities Co. Ltd, Tokyo. In accordance with FINRA Rules, you will receive an Important Disclosure Statement on an annual basis outlining the various responsibilities of MSUSA when equity products are transacted through MSUSA.

FINRA Rule 5310 – Best Execution

In any securities transaction for a customer, MSUSA will use reasonable care in seeking to obtain the most advantageous terms reasonably available under the circumstances for the execution of a customer’s order. In determining where to send customers’ orders, MSUSA takes into consideration, among other things, the size and type of order, the terms and instructions of the order, the trading characteristics of the security, the character of the market for the security, the accessibility of quotations, transaction costs, the opportunity for price or size improvement, the speed of execution, the availability of efficient and reliable order handling systems, the level of service provided by the market venue and the customer’s overall objectives with respect to the market conditions at the time of the order. MSUSA regularly reviews transactions for quality of execution.

Order Handling and Capital Commitment

The MSUSA Equity Trading Desks (“MSUSA US ET”) may maintain inventory of principal positions to provide our clients with opportunities for enhanced capital commitment. To effectively manage these inventory positions and sustain immediate liquidity for our clients, MSUSA US ET may trade out of risk resulting from customer facilitation activity at the same time we may be handling your orders at the same price level. MSUSA US ET will trade principally alongside a customer order to the extent that our principal activity either hedges or liquidates risk resulting from client facilitation. In certain instances, principal orders entered in anticipation of future client demand may also be worked concurrently with customer orders.

Regulation NMS – The Order Protection Rule was adopted to strengthen the national market system for equity securities. It requires markets to interact in a way that permits orders to seek the best available market. The Order Protection Rule (Rule 611), requires broker-dealers to prevent “trade-throughs.” Therefore, MSUSA US ET may be prohibited from effecting transactions at a price which is lower (higher) than the best bids (offers) in the market, without first accessing those better-priced protected quotations.

The Order Protection Rule contains various exceptions that, in certain situations, permit the execution of trades at prices that would otherwise constitute a trade-through. In instances where no other exceptions are available, MSUSA US ET may use an Intermarket Sweep Order (“ISO”) to sweep the market and execute any better-priced protected quotations.

In any transaction where the firm commits capital, customers may choose to decline the executions resulting from the ISOs. Whether a customer chooses to accept or decline the ISO executions, MSUSA US ET is still required to satisfy the better-priced quotations and the benefit of the resulting executions may be factored into the customer’s negotiated price. If the customer accepts the ISO executions, the transaction price received by the customer will reflect the receipt of those better-priced executions and differ from the originally negotiated price.

FINRA Rule 5320 - Trade Along, Not Held Orders

Customer orders received by MSUSA are deemed “Not Held” orders unless a customer specifically requests and provides other specific order instructions. A “Not Held” order means the customer is giving MSUSA time and price discretion in seeking to obtain the best execution for the order.

When handling “Not Held” limit orders for institutional customers, MSUSA is generally not required by regulation to display or protect the limit order. MSUSA may trade for its own account at prices equal to, or better than, those of “Not Held” orders. However, MSUSA is still obligated to provide best execution.

Handling orders on a “Not Held” basis also means that MSUSA may on occasion simultaneously conduct same-side principal trading in the same or related products while your order is outstanding. Principal trading while in possession of a customer order is allowed and may occur with knowledge of the customer order, as pre-positioning and anticipatory hedging for the overall benefit of the customer order.

MSUSA has established Information Barriers to restrict information about unexecuted orders from other trading areas not involved with the handling of the order either as an agent or as a solicited contra-party to help satisfy the no knowledge requirement.

In the case of pre-positioning or anticipatory hedging with knowledge and consideration of the customer order, an order to MSUSA may be marked as “trade-along”. MSUSA trading desks holding customer orders may be restricted from certain trading strategies in the same or related securities as the customer orders except where the pre-positioning is intended to enhance the overall execution quality for the customer. Efforts to enhance execution quality by related principal pre-positioning can occur in various circumstances.

By way of example, without limitation, when a customer seeks a guarantee to be filled at the closing price, it carries the expectation that MSUSA may engage in pre-positioning activity in order to lessen the market impact of the block, particularly on the closing price. Pre-positioning under these circumstances may diffuse the impact of a large block order by spreading out its execution effect over a period of time, and perhaps over several different markets. Further, in connection with the placement of a large ETF order where the execution of an anticipatory hedge in one or more non-option related products may serve to reduce facilitation risk and produce an overall benefit to the customer in the form of a superior execution. It should be noted that Exchange rules restrict the use of anticipatory hedges in the listed options market until after the customer’s order is publicly exposed or in the case of tied stock, where both the option order and anticipatory hedge transactions are offered to the option trading crowd.

If you choose to opt into the protections afforded by Rule 5320, please contact your MSUSA representative and/or send notice to:

Compliance Department

Mizuho Securities USA LLC

1271 Avenue of the Americas

New York, NY 10020

or by email to EQ-Compliance@mizuhogroup.com

Execution Alternatives and Sourcing Liquidity

MSUSA utilizes vendor developed tools (algorithm strategies) designed to access external and internal sources of liquidity to obtain the most favorable execution of our orders reasonably available under market conditions. These tools include smart order routers that route orders in accordance with provided instructions. These tools may also provide access to Alternative Trading Systems (“ATS”) that may provide anonymous crossing opportunities. Please note that MSUSA does not operate an ATS. MSUSA subscribes to various ATS’ and may also access such destinations via another contracted Broker Dealer. Orders worked through any of the automated execution strategies MSUSA accesses may receive automated capital provision in an attempt to improve overall execution quality. Given the variety of means that MSUSA may employ to provide orders with the best execution, and absent specific instructions to the contrary, customer transactions may be executed on an agency, agency cross, principal basis (or a combination thereof).

Market Access (SEC Rule 15c3-5)

SEC Rule 15c3-5 requires broker-dealers that access or provide access to exchanges or alternative trading systems to establish, document, and maintain a system of risk management controls that are reasonably designed to manage the financial, regulatory, and other risks in connection with market access. MSUSA has developed controls that may pause or reject select orders that exceed certain pre-determined risk parameters. For certain paused orders, MSUSA will make the determination if it is appropriate to send the orders to the market based upon a variety of factors, including, but not limited to, order size, price, and volume considerations.

Regulation NMS – Rule 605 –SEC Required Disclosure of Order Execution Information

Rule 605 states that broker dealers (market centers) must make available standardized monthly reports of statistical information concerning our equity order executions.

MSUSA Rule 605 monthly reports can be located by referencing the website http://public.s3.com/rule605/mzho/

Regulation NMS – Rule 606 – SEC Required Disclosure of Order Routing Information

Under SEC Rule 606(a), Mizuho is required to disclose, on a quarterly basis, the identity of the market centers to which it routes a significant percentage of its orders. Mizuho is also required to disclose the nature of its relationships with such market centers, including any internalization or payment for order flow and reciprocal business arrangements. MSUSA Rule 606(a) reports can be located by referencing the website http://public.s3.com/rule606/mzho/

Additionally, under SEC Rule 606(b)(1), Mizuho will provide details on NMS stock and option non-directed orders in NMS securities including the identity of the venue and the time of execution for the prior six months to clients.

Lastly, Under SEC Rule 606(b)(3) Mizuho will upon request of a client that places “Not Held” orders, provide specific disclosures regarding routing and execution of such orders for the prior six months.

To request a SEC Rule 606(b)(1) or 606(b)(3) disclosure free of charge, please send a request to 606requests@mizuhogroup.com or speak with your MSUSA business representative.

Payment for Order Flow

As a result of sending orders to certain trading centers, MSUSA may receive payment for order flow in the form of discounts, rebates, reductions of fees or credits. In certain circumstances, the amount of such remuneration may exceed the amount that MSUSA is charged by such trading centers. This does not change MSUSA’s policy to route customer orders to the trading center where it believes clients will receive the best execution, taking into account price, reliability, market depth, quality of service, speed and efficiency. Additional details are available upon request.

Regulatory Transaction Fees

Where a regulatory fee is applied to a transaction, the “fee” collected is intended to offset fees charged by various regulatory bodies. The amount collected may be more or less than the amount ultimately paid to the various regulatory bodies. In the event of the former, no reimbursement will be distributed back to you and, in the event of the latter, there will be no additional charge made to you. These fees may be detailed on the client confirmation (i.e. “SEC Section 31 FEE"). Additional information regarding any fees assessed to your transactions will be provided by Mizuho upon request.

FINRA Rule 2124 – Net Trading

At your request, MSUSA may confirm equity transaction(s) on a net basis. A net transaction is a principal transaction in which the market maker, after having received an order to buy or sell an equity security, buys or sells the security (from or to another dealer or another customer) and then sells to or buys from the customer at a different price. MSUSA is compensated in the form of a spread added to/subtracted from the cost of the position. The official confirmation for a net trade will reflect a single, all-inclusive price and will not explicitly identify the spread added/subtracted. In accordance with FINRA Rules, MSUSA will confirm your authorization orally to continue executing your orders on a net basis for each request made.

Indications of Interest

For the purpose of attracting contra side trading interest in an attempt to minimize market impact, MSUSA Equity Division may utilize certain third party vendor systems to disseminate indications of interest (“IOI”) to other market participants or trading venues. An IOI will be labeled as “natural” if it is the result of (1) an existing agency order, (2) an indication of interest to transact in a particular security other than an order (in touch with) from a customer; or (3) interest on a principal basis that is being or was established for the purpose of facilitating a client order. Resulting transactions may be executed on a principal basis, agency cross basis or a combination thereof.

Alpha Capture Systems

MSUSA Equity representatives have the ability to disseminate trade ideas to alpha capture systems (“ACS”). Under certain circumstances, MSUSA Equity representatives might deem it appropriate to share trade ideas, in whole or in part, with you and other via one or more ACS. As a result, trade ideas provided to you through those platforms may also be shared with other customers that participate in those platforms. As a registered broker-dealer, MSUSA reserves the right to review any trade idea submission and reject, close, or amend any such submission. MSUSA may today, or in the future, do business or enter into transactions on a principal basis for any issuer(s) or financial instrument(s) to which such trade idea(s) directly or indirectly relate, including in response to the trade idea(s). MSUSA employees or agents may personally hold investments or enter transactions for any issuer(s) or financial instrument(s) to which such trade idea(s) directly or indirectly relate, including in response to the trade idea(s). The trade idea(s) are prepared in accordance with MSUSA’s policy for managing conflicts of interest. If you have any questions, or have an objection to the manner in which MSUSA is handling the use of trade ideas that are submitted to ACS, please contact your MSUSA representative.

FINRA Rule 5270 – Prohibition on Front Running Client Block Transactions

Rule 5270 (the “Rule”) prohibits a broker-dealer from trading for its own account while in possession of information regarding an imminent client block transaction. MSUSA employees are generally prohibited from engaging in such activity. Rule 5270 does contain certain exceptions to this general prohibition. The Rule does not preclude a broker-dealer from trading for its own account for purposes of fulfilling or facilitating the execution of a client’s block transaction. Consistent with this exception, MSUSA may engage in trading to hedge the risk of a client’s block transaction using market data and other forms of permissible information. This hedging activity may coincidentally impact the market price of the financial instruments.. MSUSA will trade in a manner designed to limit market impact and consistent with our best execution obligations.

MSUSA will not place our financial interests ahead of our client’s in the facilitation of block transactions or other services in which MSUSA engages.

Extended Trading Hours

FINRA Rule 2265 requires that MSUSA disclose the following potential risks to customers who engage in equities transactions during extended trading hours (4:00pm – 9:29:59am Eastern Standard Time)

- Risk of Lower Liquidity. Liquidity refers to the ability of market participants to buy and sell securities. Generally, the more orders that are available in a market, the greater the liquidity. Liquidity is important because greater liquidity makes it is easier for investors to buy or sell securities. As a result, investors are more likely to pay or receive a competitive price for securities purchased or sold. There may be lower liquidity in extended hours trading as compared to regular trading hours. As a result, an order may only be partially executed, or not at all.

- Risk of Higher Volatility. Volatility often refers to the amount of uncertainty or risk related to the size of changes in a security's value. Generally, the higher the volatility of a security, the greater its price swings. There may be greater volatility in extended hours trading than in regular trading hours. As a result, orders sent during extended trading hours generally receive an inferior price than what would be received during regular trading hours.

- Risk of Changing Prices. The prices of securities traded in extended hours trading may not reflect the prices either at the close of regular trading hours, or upon the opening the next morning. As a result, orders sent during extended trading hours may receive inferior prices than what would be received during regular trading hours.

- Risk of Unlinked Markets. Depending on the extended hours trading system or the time of day, the prices displayed on a particular extended hours trading system may not reflect the prices in other concurrently operating extended hours trading systems. Accordingly, an order may receive an inferior price in one extended hours trading system than it would in another extended hours trading system.

- Risk of News Announcements. Normally, issuers make news announcements that may affect the price of their securities after regular trading hours. Similarly, important financial information is frequently announced outside of regular trading hours. In extended hours trading, these announcements may occur during trading. As a result, orders sent during extended trading hours may receive inferior prices than what would be received during regular trading hours.

- Risk of Wider Spreads. The spread refers to the difference in price between what you can buy a security for and what you can sell it for. As a result, orders sent during extended trading hours may receive inferior prices than what would be received during regular trading hours.

Large Trader Reporting

Rule 13h-1 Large Trader Reporting requires a market participant that meets the definition of a Large Trader to: (1) identify itself to the SEC via filing of the Form 13H; (2) obtain a Large Trader ID (“LTID”) from the SEC; (3) provide its LTID to all executing and clearing registered broker-dealers through whom it transacts in NMS securities and identify each account to which it applies. A Large Trader is defined as a market participant whose transactions in NMS equity securities and Listed Options for their own account or any account for which they exercise discretion equal or exceed either: (a) 2 million shares or shares with a fair market value of $20 million during any calendar day or (b) 20 million shares or shares with a fair market value of $200 million during any calendar month.

Conflict of Interest Disclosures

MSUSA provides a diverse range of financial products and services on a global basis. As such, certain conflicts of interests may arise between MSUSA and its customers and/or counterparties.

Some of the assets and instruments customers trade may include:

- Obligations sponsored or serviced by Mizuho global entities.

- Obligations of companies for which Mizuho global entity has acted as underwriter, agent, placement agent, initial purchaser or dealer or for which Mizuho has acted as lender or provided other commercial or investment banking services, or derivative instruments related to such obligations.

MSUSA may act as investor, initial purchaser, underwriter, dealer and/or placement agent in, or undertake other transactions involving, instruments discussed with a MSUSA trading or sales representatives. MSUSA may provide or have provided related derivative instruments or other related commercial or investment banking services, which may have an adverse impact on contemplated transactions. Clients or counterparties may not be informed of these other transactions. Mizhuo’s global entities or its clients may act as a counterparty to any order placed by clients. Mizuho may enter into transactions contrary to any recommendation or published views made by Mizuho. Mizuho may have short or long positions or own a material position in the subject securities. Mizuho may act as principal or agent in transactions involving the subject securities. Mizuho may enter into related derivative transactions or may solicit or perform financial or advisory services for the issuers of the subject securities or financial instruments.

MSUSA will maintain all non-public information in accordance with Mizuho’s internal policies. MSUSA may share non-public information with other Mizuho affiliates to the extent deemed necessary by Mizuho to consummate the transaction or provide the product or service contemplated. . Additionally, Mizuho may share customer confidential information with Mizuho global entities for the purpose of providing customers additional products and services. Industry regulations or existing customer agreements may prohibit “cross selling”. Should this be the case, a MSUSA representative may seek consent to share client confidential information with its affiliates for that purpose.

Notice to Canadian Customers

Please note that if you are a client domiciled in Canada, when MSUSA trades with you it does so in reliance upon the Exemption from the dealer registration requirement under NI 31-103 (as such Exemption may be amended and restated from time to time). Pursuant to the Exemption, MSUSA is subject to trading restrictions, including, among other things, that MSUSA is only permitted to trade “foreign securities” with “permitted clients” (as defined in NI 31-103) resident in Canada. A foreign security is a security issued by an issuer incorporated, formed or created under the laws of a foreign (i.e., non Canadian) jurisdiction or a security issued by a government of a foreign jurisdiction. This serves to put you on notice that you should only place orders with MSUSA for foreign securities in accordance with the Exemption.

Please click here for the names and addresses of MSUSA’s agents for service of process in the local jurisdiction

Penny Stocks

Generally, penny stocks are low-priced shares of small companies that are not traded on an exchange or quoted on Nasdaq. Penny stocks generally are traded over-the-counter, such as on the OTC Bulletin Board or Pink Sheets, and are historically more volatile and less liquid than other equities. For these and other reasons, penny stocks are considered speculative investments and customers who trade in penny stocks should be prepared for the possibility that they may lose their entire investment, or an amount in excess of their investment if they purchased penny stocks on margin. Before investing in a penny stock, you should thoroughly review the company issuing the penny stock. In addition, you should be aware of certain specific risks associated with trading in penny stocks.

Further information concerning penny stocks and the risks involved in trading them is available on the SEC's website at http://www.sec.gov/investor/pubs/microcapstock.htm.

Options Disclosure Document

Structured securities, derivatives, and options are complex instruments. They are not suitable for all investors and may involve a high degree of risk. They may only be appropriate investments for sophisticated investors who are capable of understanding and assuming the risks involved. Customers who effect transactions in listed options should receive and understand the Characteristics and Risks of Standardized Options (ODD) pamphlet prior to executions. Pursuant to SEC Rule 9b-1 and various exchange rules, MSUSA is required to provide all clients who trade options and/or who receive options-related sales material, a current copy of the ODD including supplements, issued by the Options Clearing Corporation. The pamphlet can be found on The Options Clearing Corporation’s website: http://www.theocc.com/about/publications/character-risks.jsp

Professional Customer Designation for Listed Options

MSUSA is required to review each customer’s activity on at least a quarterly basis. MSUSA is required to designate certain public customer orders as “professional orders”, where appropriate. Customer that average more than 390 orders in listed options per day during any month must be marked as professional orders for during next calendar quarter. At any time, an exchange may designate a customer as a Professional Customer where the customer has averaged more than 390 orders per day during a month. If so, the Exchange will notify MSUSA and MSUSA will be required to change the manner in which it is representing the customer’s orders within five days. To comply with this requirement,

MSUSA will mark client orders as professional customer orders should they meet the above criteria. Additionally, brokers or dealers that route listed option order flow to MSUSA are obligated to review their client’s order flow and ensure that any professional customer orders are appropriately marked.

Solicited Order Mechanisms

MSUSA must notify customers of its intent to use the solicited order mechanisms to cross customer options orders.

Cboe Exchange, Inc. – Automated Improvement Mechanism (“AIM”) AON Solicitation Mechanism.

When MSUSA handles an order of 500 contracts or more on behalf of a customer, it may solicit other parties to execute against the customer order. Thereafter, MSUSA may execute the clients order using the Cboe Exchange, Inc.’s AON AIM Solicitation Mechanism. This CBOE functionality provides a single-priced execution, unless the order results in price improvement for the entire quantity. If so, multiple prices may result. For further details, please refer to Cboe Exchange, Inc. Rule 6.74B, which is available at: https://markets.cboe.com/us/options/regulation/

Nasdaq U.S. Options Exchanges – Solicitation Order Mechanisms.

When MSUSA handles an order of 500 contracts or more on behalf of a client, it may solicit other parties to execute against your order. Thereafter, it may execute your order using the Nasdaq ISE (ISE).

*Nasdaq GEMX (GEMX) and Nasdaq MRX (MRX) Exchange’s Solicited Order Mechanisms. This functionality provides a single-price execution only. A client’s entire order may receive a better price after being exposed to the Exchange’s participants, but will not receive partial price improvement. For further details, please refer to Nasdaq ISE (ISE), Nasdaq GEMX (GEMX) and Nasdaq MRX (MRX) Rules 716(e), all which are available at http://www.ise.com/options/regulatory-and-fees/rules-and-rule-changes/.

Cboe Exchange, Inc. Tied Hedge Transactions

When MSUSA handles a listed option order of 500 contracts or more on a customer’s behalf, it may buy or sell a hedging stock, futures position following receipt of the option order prior to announcing the option order to the trading crowd. Thereafter, MSUSA may execute the option order using the tied hedge procedures of the exchange on which the order is executed. These procedures permit the option order and hedging position to be presented for execution as a net-priced package subject to exchange requirements. For further details, please refer to NYSE Arca Rule 6.74, NYSE AMEX Rule 934.3, CBOE Rule 6.74.10, which is available on the NYSE website www.nyse.com and CBOE’s website at: www.cboe.org/legal.

Position Limits

Position limits on the maximum number of equity and index exchange listed and over-the-counter (OTC) put and call options covering the same underlying security that may be held or written by a single investor (or group of investors acting in concert or under common control). This is regardless of whether the options are purchased or written on the same or different exchanges or are held or written in one or more accounts or through one or more brokers. Under the terms of the MSUSA Listed Options Agreement, clients agree not to violate these limits and authorize MSUSA to take action to bring the client’s positions into compliance with regulatory requirements. MSUSA must monitor and report a client’s positions to the options regulators and may be required to liquidate positions in excess of these limits. If MSUSA fails to adhere to these regulations, it may be subject to the imposition of fines and other regulatory actions. The position limit applicable to a particular option class is determined by the options exchanges and is based on the number of shares outstanding and trading volume of the security underlying the option. Positions are calculated on both the long and short side of the market. A long position includes the aggregate of both calls purchased (long calls) and puts written (short puts), on the same underlier. A short position includes the aggregate number of calls written (short calls) and puts purchased (long puts) on the same underlier OTC option positions are calculated separately from listed option positions. Further, there are position limits for OTC options on non-U.S. listed equity securities for accounts held by U.S. broker-dealers. Expiring options are included in your end of day position.

Options positions under common control for all accounts are aggregated as follows:

For example, if the limit on a particular option class is 250,000 contracts, an investor or group of investors acting in concert or under common control (i.e., same order placer or ultimate decision maker) may purchase up to 250,000 listed calls on a particular underlying security, and at the same time, write up to 250,000 listed calls covering the same underlying security (long call and short call positions are on opposite sides of the market and are not aggregated for purpose of position limits). An investor or group of investors acting in concert or under common control that purchased 125,000 listed puts on a particular underlying security may at the same time, write up to but no more than 125,000 listed calls covering the same underlying security (long put and short call positions are on the same side of the market, and are aggregated for purposes of the limits) without exceeding the position limit for the security. In addition, the same investor or group of investors acting in concert or under common control may purchase or write up to 250,000 OTC options on the same side of the market without exceeding the position limits for the underlying security.

The position limit rules also permit positions in excess of the applicable limit when the client is engaging in certain qualified hedging strategies. These exemptions can be found in each exchange’s rules. For example, Cboe Exchange, Inc. Rules 4.11, 20.6, 22.6, 23.3, 24.4, 24.4A, 24.4B, 24.4C and 24A.7 Position Limits, Rule (link: https://markets.cboe.com/us/options/regulation/) and FINRA Rule 2360 Options (link: https://www.finra.org/rules-guidance/rulebooks/finra-rules/2360) discuss the qualified hedge strategies in detail. Clients must determine the current position limits from their brokers or the Options Clearing Corporation Website (http://www.optionsclearing.com) before engaging in any options transactions.

Exercise Limits

Exercise limits restrict the maximum number of equity and index listed and OTC options covering the same underlying security that can be exercised within any five (5) consecutive business days. This limit is imposed on a single investor or group of investors acting in concert or under common control (regardless of whether the options are purchased or written on the same or different exchanges or are held or written in one or more accounts or through one or more brokers). The exercise limit is the same as the position limit for the underlying security. If a client has an open option position that is above the established position limit, but has a qualified hedge strategy, they are permitted to exercise the amount of options for which they are fully hedged within any five (5) consecutive business day period.

Fails Charges

MSUSA may assess counterparties a standardized “Fails Charge” in connection with delivery failures for any delivery-versus-payment (DVP) or delivery-versus-transfer (DVT) transactions, unless otherwise agreed to for a particular transaction. This policy covers, but is not limited to, both $U.S. Dollar-denominated ($USD) and Japanese Yen-based (¥JPY) securities products. This charge is designed to help reduce fails in the marketplace, and to promote efficient market clearing and overall market liquidity. It is also designed to compensate the non-failing counterparty for the potential economic harm resulting from the fail (which is often difficult to ascertain). By entering into any transaction with MSUSA (including any cash purchase or sale, forward purchase or sale, option, repurchase (“repo”) or reverse repo transaction, or bonds borrow or loan transaction), the counterparty will be deemed to have agreed that such transaction will be subject to a potential Fails Charge. MSUSA’s failure to enforce any such Fails Charge in any one transaction or in multiple transactions shall not constitute a waiver of the foregoing rights with regard to any other transactions subject to a Fails Charge. Further, the assessment of any Fails Charge shall be without prejudice to any other rights or remedies under the applicable agreement governing the transaction or applicable law, and shall not constitute a waiver of the non-failing party’s right to exercise any other remedy. Alternatively, MSUSA may also be willing to cash settle failing transactions on mutually agreeable terms. For additional information on specific asset classes, please also see:

- US Treasury Securities. The Treasury Market Practices Group (the “TMPG”) and the Securities Industry and Financial Markets Association (“SIFMA”) have published a “U.S. Treasury Securities Fails Charge Trading Practice” that covers MSUSA’s US Treasury transactions with its counterparties. Any delivery-versus-payment or delivery-versus-transfer transaction in any covered product under these guidelines, including US Treasury securities, between MSUSA and our counterparties is deemed to be subject to this Fails Charge Trading Practice.

- Japanese Government Securities (JGBs). The Japan Securities Dealers Association (“JSDA”) publishes the Japanese Government Securities Guidelines for Real Time Gross Settlement and its related “Guidelines for Practical Handling of Fails Charges”. This document in its entirety can be found on the JSDA’s website. MSUSA may assess a fails charge for any transactions in Japanese government securities based on DVP settlements.

MSRB Rule G10 Investor Education and Protection

The Municipal Securities Regulatory Board (“MSRB”) under Rule G10 requires MSUSA to notify customers of the following:

- MSUSA is registered with the Securities and Exchange Commission (“SEC”) and the MSRB. As such, MSUSA is subject to the regulations and rules on the municipal securities activities established by the SEC and MSRB

- The website for the SEC is www.sec.gov and the website for the MSRB is: www.msrb.org

- A Municipal Securities Investor Information Brochure is available free of charge at https://msrb.org/msrb1/pdfs/msrb-investor-brochure.pdf

Municipal Advisor Disclosure

The Dodd-Frank Wall Street Reform and Consumer Protection Act (“Dodd Frank”) and the Securities Exchange Act of 1934 (“Exchange Act”) require that certain financial entities register as “municipal advisors,” depending on the actives of their clients. The requirement covers firms that either: (1) provide advice to or on behalf of a municipal entity or obligated person with respect to municipal financial products or the issuance of municipal securities, including advice with respect to the structure, timing, terms, and other similar matters concerning such financial products or issues; or (2) undertakes a solicitation of a municipal entity or obligated person. “Municipal financial products” include municipal derivatives, guaranteed investment contracts, and investment strategies (including importantly plans or programs for the investment of proceeds of municipal securities; or the recommendation of municipal escrow investments). The requirements are intended to mitigate certain “pay to play” practices, undisclosed conflicts of interest, inadequate advice, and failures to place the duty of loyalty to their clients ahead of the firm’s own interests. During the financial crisis, a number of municipalities suffered losses from complex derivatives products that were marketed by unregulated financial intermediaries.

Mizuho Securities USA LLC is not an “investment adviser” registered under the Investment Advisers Act of 1940, a registered municipal advisor under the Exchange Act, and does not intend to register as an investment advisor nor as a municipal advisor in the future. MSUSA will not provide you any advice concerning municipal financial products or the issuance of municipal securities, including the investment of proceeds of municipal securities, investment of other funds of a municipal entity, guaranteed investment contracts or the use of municipal derivatives. By accepting this notice, MSUSA customers acknowledge that:

- You qualify as an Institutional Investor and/or a Sophisticated Municipal Market Professional (“SMMP”) under the applicable industry standards. As such, you exercise independent judgment and are fully capable of evaluating the quality of secondary market transactions, and/or evaluating any information provided by MSUSA, including the investment risks and market value of particular transactions and investment strategies. You do not receive (and you do not expect MSUSA to provide) any information that is otherwise reasonably accessible to the institutional market, and/or to undertake any customer-specific suitability obligations.

- MSUSA acts as a securities dealer. You trade with MSUSA acting as principal for its own account, on a Receipt-Against-Payment/Deposit-Against-Payment (“RVP/DVP”) basis. When MSUSA acts as the principal to a trade, it will use its own inventory to fill your client orders. You wish to continue to trade with MSUSA as principal basis.

- MSUSA does not provide you any advice with respect to municipal financial products or the issuance of municipal securities, including municipal derivatives, guaranteed investment contracts, or the investment of proceeds of municipal securities. MSUSA may provide customers certain ongoing securities market information (either in writing or in oral communications), but does not provide any “advice” that would otherwise require MSUSA’s registration as a municipal advisor. Accordingly, MSUSA does not provide clients , without limitation, any ‘recommendations’ that are particularized to your specific investment needs, objectives, or circumstances with respect to municipal financial products or the issuance of municipal securities and MSUSA does not owe clients a fiduciary duty pursuant to Section 15B of the Exchange Act. MSUSA may provide general financial and investing information, including information of a factual nature that does not include any tailored, subjective assumptions, opinions, or views, or information that is particularized to a client’s specific investment needs. This type of general information may include, and is typically limited to general market and financial information (including e.g., information concerning current market interest rates or index rates for different types of bonds or categories of credits; information regarding investments (e.g., the terms, maturities, and interest rates at which MSUSA offers these investments); price quotes; axes for investments available for purchase or sale; factual information describing various types of debt financing structures (e.g., fixed rate debt, variable rate debt, general obligation debt, debt secured by various types of revenues, or insured debt); or comparisons of the general characteristics, risks, advantages, and disadvantages of certain debt financing structures. This information is typically available to all Mizuho clients, and is not particularized to a specific client’s needs. It is factual in nature, and does not contain or express subjective assumptions, opinions, or views, or constitute a recommendation. Clients should not view any information received from MSUSA as a suggestion to take action or refrain from taking action. Client’s should not deem this information to imply a recommendation or otherwise constitute advice. Clients are encouraged to discuss any information or material provided by MSUSA with any and all internal or external advisors and experts that they deem appropriate before acting on any such information.

d. Business Continuity Disclosure

In accordance with FINRA Rule 4370, MSUSA has developed and implemented a Business Continuity Plan (“BCP”) designed to address and mitigate the potential consequences of a significant business disruption.

Our BCP is intended to permit the temporary continuation of the key parts of our business despite the occurrence of a significant business disruption with a goal of recovering the key aspects of our business within twenty four hours or less. Our BCP also is designed to safeguard employees, protect our books and records, and provide ready access for our clients to any securities and/or funds in the custody of MSUSA’s bank depositories in the event that we are unable to achieve a timely recovery.

MSUSA’s BCP attempts to anticipate the various types of events that could interfere with our ability to operate on a normal basis. Staff have been assigned to specific recovery responsibilities and trained in special procedures to be followed should an event occur that could cause a disruption to occur. MSUSA has deployed an overlapping communications triangle that connects three geographically diverse locations to ensure flexibility and redundancy in our ability to communicate internally and externally. All mission critical systems have been duplicated in each of our data centers with data backed up electronically on a near synchronized basis at locations over 700 miles apart and also duplicated in physical form and sent to secure off-site facilities at the end of each business day. We also have deployed redundant communication lines from multiple locations with industry utilities, information providers, and clearing organizations. We have established alternative methods to communicate with our employees, clients and regulators.

We believe that our BCP meets or exceeds all industry standards and regulatory requirements. We further believe that we have implemented reasonable and prudent measures to overcome or at least mitigate the consequences of an event that would otherwise interfere with the normal course of our business. However, because it is not possible to anticipate the nature, scope, impact and consequence of every possible business disruption, MSUSA does not represent or guaranty that it will be able to continue or resume business operations within any specified period of time under all circumstances.

Our BCP is subject to periodic modification. A copy of the summary of our BCP is available upon request by writing to:

Mizuho Securities USA LLC

Attn: Chief Operating Officer

1271 Avenue of the Americas

New York, New York 10020

e. Futures Specific Disclosures

Please Click here for futures specific disclosures, including the 1.55(O) Financial information as well as the 1.55(K) Firm-specific disclosures.

f. MSUSA Statement of Financial Condition

Copies of MSUSA’s audited financial statements will be provided upon request by any customer (as defined in FINRA Rule 2261).

MSUSA’s most recent financial statements can be viewed using the links below:

- March 31, 2026

- September 30, 2025

- March 31, 2025

- September 30, 2024

- March 31, 2024

- September 30, 2023

- March 31, 2023

- September 30, 2022

- March 31, 2022

- September 30, 2021

- March 31, 2021

- September 30, 2020

- March 31, 2020

- September 30, 2019

- March 31, 2019

- September 30, 2018

g. Sales of Investment Products to Customers of Mizuho Bank (USA).

Investment products offered through MSUSA to customers of Mizuho Bank (USA):

h. Collateral Arrangements

An Information Statement has been prepared to comply with Article 15 of the Securities Financing Transactions Regulation by informing customers of the general risks and consequences that may be involved in consenting to a right of use of collateral provided under a security collateral arrangement or of concluding a title transfer collateral arrangement. The information statement can be located at https://www.icmagroup.org/assets/documents/Maket-Practice/Regulatory-Policy/Repo-Markets/SFTR-Information-Statement-May-13-2016.pdf

2. Mizuho Capital Markets LLC (“MCM”)

MCM is registered with the Commodity Futures Trading Commission (“CFTC”) as a US Swap Dealer pursuant to Title VII of the Dodd-Frank Wall Street Reform and Consumer Protection (“Dodd-Frank”) Act. The Dodd-Frank Act creates a comprehensive regulatory framework that, among other things, requires that swap dealers make certain disclosures of material information to their swaps counterparties prior to entering into a swap with that counterparty.

MCM is registered with the Securities Exchange Commission (“SEC”) as a Security-Based Swap Dealer (“SBSD”) pursuant to 17 CFR Part 240. The following disclosures are provided to you in accordance with the requirements set forth in § 240.15Fh-3 of the SEC rules in connection with any security-based swap transaction.

a. General Risk Disclosures and Asset Specific Disclosures

ISDA Standard Disclosures

The International Swaps and Derivatives Association (“ISDA”) maintains the disclosures required by CFTC Rule 23.431(a) and SEC rule 240.15Fh-3(b). These disclosures are updated from time to time, and may be found on ISDA’s website at the following URL: https://www2.isda.org/functional-areas/legal-and-documentation/disclosures/. Prior to executing a swap with MCM, we ask that you review the most recent Updated General Disclosure Statement, which will contain general disclosures regarding certain risks associated with executing a swap transaction. We also ask that you review the most recent asset-specific disclosure annex for interest rate and/or foreign exchange derivatives as applicable to your anticipated trading activity, including without limitation, the IBOR Alternative Reference Rates Disclosure for Interest Rate Transactions.

The latest published documents are attached below:

General Disclosures Document

Credit Derivatives Disclosure

Equity Derivatives Disclosure

Foreign Exchange Derivatives Disclosure

Interest Rate Derivatives Disclosure

IBOR Alternative Reference Rates Disclosure for Interest Rate Transaction

Mizuho FX Market Making Disclosures

Mizuho provides its clients with additional disclosures regarding its foreign exchange market making business. These disclosures supplement the ISDA Standard Disclosures provided above and should be read in conjunction with those disclosure. Mizuho’s FX Market Marketing Disclosures can be found here.

b. Initial Margin Segregation Disclosure

CFTC Rule 23.701 and SEC Rule § 240.18a-1 requires that we notify you, to the extent that you post Initial Margin in respect of an Uncleared Swap, that you have the right to elect to have that Initial Margin segregated in accordance with the requirements of CFTC Rules 23.702 and 23.703. Capitalized terms, as used herein, are defined in CFTC Rule 23.700.

If you would like further information on this offering, please contact usderivsonboarding@mizuhogroup.com.

c. Daily Mark Disclosures

If required by CFTC rule 23.431(d)(3) and SEC rule 240.15Fh-3(c)(2), we will provide you with a daily mark for all uncleared swaps not subject to daily variation margining, and/or all uncleared security-based swaps. Such daily mark may not necessarily (i) be a price at which either we or you would agree to replace or terminate such swap or security-based swap; (ii) unless otherwise expressly agreed, be the basis for margin calls and maintenance of collateral, if any; and (iii) be the value of the transaction that is marked on our books and records. The daily mark will be provided to you at such address we have on record or as you otherwise advise to us by communication to Derivs-FIMOUS@mizuhogroup.com.

For cleared swaps executed between you and MCM, upon request, you have the right to receive a daily mark from the relevant derivatives clearing organization, in accordance with CFTC rule 23.431(d)(1).

For cleared security-based swaps executed between you and MCM upon request, you have the right to receive the daily mark that the security-based swap dealer receives from the appropriate clearing agency through which you clear such security-based swaps, in accordance with SEC rule 240.15Fh-3(c)(1).

Additional disclosures on the daily mark methodology and assumptions can be found here.

d. Right to Select the Clearinghouse

You have the sole right to select the DCO at which a swap will be cleared for any swap entered into between you and MCM that is subject to the mandatory clearing requirements under Sections 2(h) and 3C(a) of the Commodity Exchange Act.

You may elect to clear any swap and have the sole right to select the DCO at which the swap will be cleared with respect to any swap entered into between you and MCM that is not subject to the mandatory clearing requirements under Sections 2(h) and 3C(a) of the Commodity Exchange Act.

With respect to any Security-Based Swap entered into between you and MCM that is subject to the mandatory clearing requirements under Section 3C(a) of the Securities Exchange Act, you have the sole right to select the clearing agency at which the Security-Based Swap will be cleared, in accordance with SEC Regulation 240.15Fh-3(d)(1). For a general list clearing agencies that clear security-based swaps and which security-based swaps each clearing agency clears, please refer to the list published by ISDA here: https://www.isda.org/2021/05/03/current-security-basedswap-clearing/. Of those clearing agencies, MCM is authorized or permitted, directly or through a designated clearing member, to clear Security-Based Swaps at the following: ICE Clear Credit LLC and LCH SA.

With respect to any Security-Based Swap entered into between you and MCM that is not subject to the mandatory clearing requirements under Section 3C(a) of the Exchange Act, but may be accepted for clearing by one or more clearing agency as determined by MCM, you may elect to clear such Security-Based Swap. If you elect to clear such Security-Based Swap, you have the sole right to select the clearing agency through which to clear, so long as it is one of the clearing agencies at which MCM is authorized or permitted, directly or through a designated clearing member, to clear the applicable Security Based Swap, in accordance with SEC Regulation 240.15Fh-3 (d)(2)(iii). For a general list clearing agencies that clear security-based swaps and which security-based swaps each clearing agency clears, please refer to the list published by ISDA here: https://www.isda.org/2021/05/03/current-security-based-swap-clearing/. Of those clearing agencies, MCM is authorized or permitted, directly or through a designated clearing member, to clear Security-Based Swap at the following: ICE Clear Credit LLC and LCH SA.

e. Special Entities

If you are an employee benefit plan as defined in Section 3 of Employee Retirement Income Security Act (“ERISA”) that is not subject to the Title 1 of ERISA then MCM hereby notifies you of your right to elect to be treated as a special entity pursuant to CFTC rule 23.430(c) and SEC rule 240.15Fh-3(a)(3).

f. Potential Conflicts of Interest

If MCM determines that it may have a conflict of interest in connection with a particular swap and/or security-based swap or that it may have received compensation of other material incentives from a source other than the counterparty to the swap and/or security-based swap in connection with such swap and/or security-based swap, MCM will notify the counterparty of such apparent conflict of interest or material incentive prior to entering into such swap and/or security-based swap. If any such potential conflict of interest involves “Exposure Hedging” or “Pre-Hedging Transactions,” as defined and discussed in Mizuho Americas Pre-Hedging Disclosure, that Disclosure shall serve as MCM’s disclosure of any potential conflict.

g. Alternative Compliance Mechanism.

MCM is operating under 17 CFR 240.18a-10 (the “Alternative Compliance Mechanism”) and is therefore complying with the applicable capital, margin, segregation, recordkeeping, and reporting requirements of the Commodity Exchange Act and the rules promulgated by the U.S. Commodity Futures Trading Commission thereunder in lieu of complying with the capital, margin, segregation, recordkeeping, and reporting requirements promulgated by the U.S. Securities and Exchange Commission in 17 CFR 240.18a-1 and 17 CFR 240.18a-3 through 17 CFR 240.18a-9.

h. MCM Statement of Financial Condition

Click below to view MCM's most recent financial statements.

- March 31, 2026

- September 30, 2025

- March 31, 2025

- September 30, 2024

- March 31, 2024

- September 30, 2023

- March 31, 2023

- September 30, 2022

- March 31, 2022

- March 31, 2021

i. Portfolio Reconciliation

In accordance with SEC Rule § 240.15Fi-3(b) and CFTC 23.502(b), MCM has established, maintains, and follows policies and procedures reasonably designed to ensure it engages in portfolio reconciliation for security-based swap and swaps. With respect to the trade data provided to you as part of this process, if you do not respond within the five business days, you are deemed to have reviewed and agreed to the accuracy of the trade data. If you do identity discrepancies with your trade data, please reach out to MCM as soon as possible.

j. After Hours Orders

A customer of Mizuho Capital Markets LLC (MCM) may submit a trade request or respond to a quote after the close of business New York time via email, phone, or chat. MCM is not under any obligation to accept or act upon any trade request submitted after the close of its business in New York time. If a trade request is submitted to MCM after the close of business for an execution at market, MCM may execute the order at the open of business New York time the following business day and will provide a post trade recap providing the market prices. Due the nature of the FX market and in periods of extreme market volatility, MCM is not under any obligation to execute an order at the price quoted on the previous New York business day. Drawdowns for Window Forwards submitted to MCM after the close of MCM’s business day in New York are not accepted until the following business day.

k.Disclosure and Notice for Canadian Counterparties

Pursuant to Section 39(2)(b) of the Canadian Multilateral Instrument 93-101 Derivatives: Business Conduct and the national instrument that succeeds MI 93-101 following the adoption of a substantially similar rule to MI 93-101 by the British Columbia Securities Commission (the “Business Conduct Rule”). MCM is a foreign derivatives dealer under the Business Conduct Rule and will be relying on the exemption set out in Section 39 of the Business Conduct Rule. MCM hereby provides notice of the following information:

- (i) The head office or principal place of business of the Foreign Dealer is located in the following foreign jurisdiction: United States of America

- (ii) All or substantially all of the assets of MCM may be situated outside of any Canadian local jurisdiction.

- (iii) There may be difficulty enforcing legal rights against MCM because of the above.

Please click here for the names and addresses of MCM’s agents for service of process in the local jurisdiction

l. Contact Information

Should you have any additional questions regarding these disclosures, please contact onboarding@mizuhogroup.com. Complaints may be directed to:

Mizuho Capital Markets LLC

1271 Avenue of the Americas

New York, NY 10020

Attn: Chief Compliance Officer

+1 (212) 547-1500

customerservice@mizuhocap.com

3. Mizuho Bank (USA) (“BKUSA”)

BKUSA is a New York State-chartered bank and is a member of the Federal Reserve System and of the Federal Deposit Insurance Corporation (“FDIC”). BKUSA is supervised by the New York State Department of Financial Services and the Board of Governors of the Federal Reserve System.

BKUSA accepts deposits from institutional clients through a variety of channels, including the Mizuho Americas Treasury Services platform. Deposits placed with BKUSA are insured up to certain coverage limits. The current standard maximum deposit insurance amount is $250,000 per depositor. For more information regarding FDIC deposit insurance coverage, visit www.fdic.gov.

BKUSA also offers certain non-deposit investment products. Non-deposit products are not insured by the FDIC; are not deposits or other obligations or BKUSA and are not guaranteed by BKUSA; and are subject to investment risks, including possible loss of the principal invested.

Investment products offered by BKUSA:

BKUSA maintains representative offices in Chicago, Illinois; Atlanta, Georgia; Houston, Texas; Los Angeles, California; and San Francisco, California.

a. Community Reinvestment Act (“CRA”) Rating Statement

BKUSA has received an “Outstanding” CRA rating for meeting the needs of its community, particularly in low- and moderate-income neighborhoods through community development loans, investments, grants and services.

b. Bank Secrecy Act/Anti-Money Laundering Disclosure

The policy of BKUSA is to prohibit and actively prevent money laundering and any activity that facilitates money laundering or the funding of terrorist or criminal activities.

In order to guard against money laundering and terrorist financing, the Bank Secrecy Act (“BSA”) requires financial institutions, including BKUSA, to establish a written anti-money laundering program reasonably designed to assure and monitor compliance with the provisions of the BSA. At a minimum, the anti-money laundering program must provide for: (i) the appointment of a compliance officer; (ii) a system of internal controls designed to ensure compliance with the BSA; (iii) training for appropriate personnel; and (iv) an independent testing of BSA compliance.

To help the US government fight the funding of terrorism and money laundering activities, federal law requires all financial institutions to obtain, verify and record information that identifies each person and entity that opens an account.

When you open an account, we will ask for certain information, including your full legal name, physical business address, tax identification number and other information that will allow us to identify you. We may also seek to see your legal organizational documents, financial statements or other identifying documents, among other things.

4. Mizuho Bank, Ltd. (“MB”)

MB is a foreign banking organization organized under the laws of Japan. MB maintains state-licensed branch offices in New York, New York; Chicago, Illinois; and Los Angeles, California and representative offices in Atlanta, Georgia; Houston, Texas; and San Francisco, California. MB is supervised by the states in which it maintains offices, the Board of Governors of the Federal Reserve System, and the Financial Services Agency of The Government of Japan. MB is not a member of the Federal Deposit Insurance Corporation (“FDIC”).

MB accepts deposits from institutional clients through a variety of channels, including the Mizuho Americas Treasury Services platform. MB does not accept deposits from the general public, and deposits placed with MB at or through any of its three US branches are not insured by the FDIC.

USA PATRIOT Act Certification

Click here to link to the MB Global Certification Regarding Correspondent Accounts for Foreign Banks.

Should you have any questions regarding this Certification, please contact:

Aaron Wolf, Aaron.Wolf@mizuhogroup.com or

Arti Amin, Arti.Amin@mizuhogroup.com.

5. Mizuho Securities Canada Inc. (“MSCN”)

Mizuho Securities Canada Inc. (MSCN), a wholly owned subsidiary of Mizuho Securities USA LLC, conducts securities business in Canada as a registered investment dealer in each Canadian province and territory. MSCN is a member of the Canadian Investment Regulatory Organization and a member of the Canadian Investor Protection Fund. In the US, MSCN is a member of the Financial Industry Regulatory Authority.

Click below to view MSCN’s most recent financial statements.

- March 31, 2026

- September 30, 2025

- March 31, 2025

- September 30, 2024

- March 31, 2024

- September 30, 2023

- March 31, 2023

- September 30, 2022

- March 31, 2022

- September 30, 2021

- March 31, 2021

Please direct all inquiries regarding the MSCN Compliance Program, including any complaints to:

Nick Pomponio

Chief Compliance Officer

Mizuho Securities Canada Inc.

100 Yonge St. Suite 1100

Toronto, Ontario M5C 2W7

Canada

nick.pomponio@mizuhogroup.com

416 874-1148

6. Mizuho Markets Americas ("MMA")

Mizuho Markets Americas LLC (“MMA”), a Delaware limited liability company, participates in the purchase and sale of equity derivatives and is registered with the Securities and Exchange Commission as an Over-the-Counter derivatives dealer.

Click below to view MMA’s most recent financial statements.

- March 31, 2026

- September 30, 2025

- March 31, 2025

- September 30, 2024

- March 31, 2024

- September 30, 2023

- March 31, 2023

- September 30, 2022

- March 31, 2022

- September 30, 2021

- March 31, 2021

- September 30, 2020

7. GREENHILL REGULATORY DISCLOSURES (FOR ALL ENTITIES)

Greenhill & Co., Inc. and all its subsidiaries("Greenhill", the "Company" or the “Firm”) provides this website (together with its contents and all sub-websites, this "website"), for your informational purposes only.

The information, products and services on this web site are provided on an "AS IS," "WHERE IS" and "WHEREAVAILABLE" basis. Greenhill does not warrant the information or services provided herein or your use of this web site generally, either expressly or impliedly, for any particular purpose and expressly disclaims any implied warranties, including but not limited to, warranties of title, non-infringement, merchantability or fitness for a particular purpose. Greenhill will not be responsible for any loss or damage that could result from interception by third parties of any information or services made available to you via this web site. Although the information provided to you on this website is obtained or compiled from sources we believe to be reliable, Greenhill cannot and does not guarantee the accuracy, validity, timeliness or completeness of any information or data made available to you for any particular purpose. Neither Greenhill, nor any of its affiliates, directors, officers or employees, nor any third party vendor, will be liable or have any responsibility of any kind for any loss or damage that you incur in the event of any failure or interruption of this web site, or resulting from the act or omission of any other party involved in making this web site, the data contained herein or the products or services offered on this web site available to you, or from any other cause relating to your access to, inability to access, or use of the web site or these materials, whether or not the circumstances giving rise to such cause may have been within the control of Greenhill or of any vendor providing software or services. In no event will Greenhill or any such parties be liable to you, whether in contract or tort, for any direct, special, indirect, consequential or incidental damages or any other damages of any kind even if Greenhill or any other such party has been advised of the possibility thereof. This limitation on liability includes, but is not limited to, the transmission of any viruses which may infect a user's equipment, failure of mechanical or electronic equipment or communication lines, telephone or other interconnect problems (e.g., you cannot access your internet service provider), unauthorized access, theft, operator errors ,strikes or other labor problems or any force majeure. Greenhill cannot and does not guarantee continuous, uninterrupted or secure access to the web site.

None of the information contained in this web site constitutes a recommendation, solicitation or offer by Greenhill or its affiliates to buy or sell any securities, futures, options or other financial instruments of any person or provide any investment advice or service.

Proprietary Rights

All right, title and interest in this web site and any content contained herein is the exclusive property of Greenhill, except as otherwise stated. Unless otherwise specified, this web site is for your personal and non-commercial use only and you may print, copy and download any information or portion of this web site for your personal use only. You may not modify, copy, distribute, transmit, display, perform, reproduce, publish, license, frame, create derivative works from, transfer, or otherwise use in any other way for commercial or public purposes in whole or in part any information, software, products or services obtained from this web site, except for the purposes expressly provided herein, without Greenhill's prior written approval. If you copy or download any information or software from this web site, you agree that you will not remove or obscure any copyright or other notices or legends contained in any such information.

Greenhill, the Greenhill logo and other Greenhill trademarks and service marks referenced herein are trademarks and service marks of Greenhill. The names of other companies and third-party products or services mentioned herein may be the trademarks or service marks of their respective owners. You are prohibited from using any marks for any purpose including, but not limited to use as metatags on other pages or sites on the World Wide Web without the written permission of Greenhill or such third party, which may own the marks.

Use of Links

This web site contains links to third party web sites. These links are provided only as a convenience. The inclusion of any link is not and does not imply an affiliation, sponsorship, endorsement, approval, investigation, verification or monitoring by Greenhill of any information contained in any third party website. In no event shall Greenhill be responsible for the information contained on that site or your use of or inability to use such site. You should also be aware that the terms and conditions of such site and the site's privacy policy may be different from those applicable to your use of this web site.

Regulatory Matters

US Users

Greenhill provides independent financial advice on significant mergers, acquisitions, financings, restructurings, capital raisings and similar corporate finance matters. Greenhill is not a retail broker-dealer. The Firm does not conduct underwriting activities, provide research or analyst reports or solicit or carry accounts for, or offer or sell securities products to, retail customers. Greenhill & Co., LLC is registered as a broker-dealer with the Securities and Exchange Commission (“SEC”) and is regulated by the Financial Industry Regulatory Authority, Inc. as a FINRA Member Firm (http://www.finra.org/),and is licensed in all 50 states, Puerto Rico and the District of Columbia.

The information and services provided on this web site are not provided to and may not be used by any person or entity in any jurisdiction where the provision or use thereof would be contrary to applicable laws, rules or regulations of any governmental authority or regulatory or self-regulatory organization or where Greenhill is not authorized to provide such information or services.

European Users

In the UK, this website and the information contained in it (this “Website”) are made available by Greenhill & Co. International LLP (a limited liability partnership registered in the UK, no. OC332045), whose registered office is: Berkeley Square House, London W1J 6BY. Greenhill & Co. International LLP is regulated by the Financial Conduct Authority (the “FCA’’) with Firm Reference Number 474168.

In Germany, this website is made available by Greenhill Europe GmbH & Co. KG, registered with the commercial register Frankfurt HRA 50593, whose registered address is: Neue Mainzer Strasse 52, 60311 Frankfurt, Germany. Greenhill Europe GmbH & Co KG is regulated by BaFin with BaFin ID 10156408.

Greenhill may provide services in other European countries in accordance with BaFin’s passporting regime, in accordance with its permissions specified on the Financial Services Register and applicable law and regulation.

This website is provided for informational purposes only and is not directed at, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any jurisdiction (including the UK or any European country) where such distribution, publication, availability or use would be contrary to applicable law or regulation or which would subject that Greenhill and/or its subsidiaries or affiliates to any registration or licensing requirements with such jurisdiction.

Information according to Regulation (EU) 2019/2088 (SFDR):

Manner in which sustainability risks are included

Greenhill Europe does not consider sustainability risks to be of specific relevance to its investment advisory services. It is assumed that the issuers or manufacturers of the financial products to which Greenhill Europe’s advisory services relate, already take such considerations into account. Otherwise, the pre‐contractual disclosures for such financial product will include a corresponding statement in accordance with the Regulation on Sustainability‐related Disclosures in the Financial Services Sector (SFDR).

Impact of sustainability risks on returns

Greenhill Europe cannot exclude the possibility that the occurrence of sustainability risks may have a negative impact on the return of the financial product to which Greenhill Europe’s advisory services relate. This applies even if the client wishes sustainability risks to be taken into account in the investment advice. Therefore, Greenhill Europe does not calculate any risks individually.

Australian Users

Greenhill& Co. Australia Pty Limited (ABN 89 086 678 346) holds Australian financial services license no. 224482. Its advisory services are available only to “wholesale clients” within the meaning of the Corporations Act 2001 (Cth).Nothing in the above disclaimer excludes, restricts or modifies a warranty, guarantee, right or liability to the extent that to do so would be in breach of Australian law. To the maximum extent permitted by law, Greenhill limits its liability for breach of a non-excludable warranty, guarantee or right to resupplying its services or payment of the cost of resupplying its services. No Greenhill company is regulated by the Australian Prudential Regulation Authority as an Authorised Deposit-taking Institution.

Canadian Users

In connection with its capital raising services for private equity and real estate funds and sponsors, Greenhill & Co., LLC relies on the international dealer registration exemption provided in section 8.18 of National Instrument 31-103,as amended, in each of Alberta, British Columbia, Manitoba, New Brunswick, Ontario and Québec (each, a “Local Jurisdiction”) solely to “permitted clients”. Please note that: (i) Greenhill & Co., LLC is not registered in the Local Jurisdiction and will be relying on the international dealer exemption in section 8.18 of NI 31-103 to provide securities trading services to you; (ii) Greenhill & Co., LLC’s head office is located in New York, New York, the United States of America; (iii) all, or substantially all, of Greenhill & Co., LLC’s assets may be situated outside of Canada; (iv)you may have difficulty enforcing legal rights against Greenhill & Co., LLC because of the above; and (v) Greenhill & Co., LLC has appointed the following agents for service of process in each Local Jurisdiction: Alberta - Lawson Lundell LLP, Suite 3700, 205 - 5th Avenue S.W., Bow Valley Square 2, Calgary, Alberta T2P 2V7, Attention: John Christian; British Columbia - Lawson Lundell LLP, Suite 1600 Cathedral Place, 925 West Georgia Street, Vancouver, British Columbia V6C 3L2, Attention: John Christian; Manitoba - Thompson Dorfman Sweatman LLP, 2200 - 201 Portage Avenue, Winnipeg, Manitoba R3B 3L3, Attention: Bruce S. Thompson; New Brunswick - Stewart McKelvey, 10th Floor, Brunswick House, 44 Chipman Hill, PO Box 7289, RPO Brunswick Square, Saint John, New Brunswick E2L 4S6, Attention: C. Paul W. Smith; Ontario - Greenhill & Co. Canada Ltd., 79 Wellington Street West, Suite 3403, P.O. Box 333, Toronto, Ontario M5K 1K7, Attention: Bradley Crompton; Québec - BCF LLP, 1100 René Lévesque Blvd. West, 25th Floor, Montreal, Quebec H3B 5C9, Attention: Michel Rochefort.

Hong Kong Users