Colin Asher, Senior Economist. European Treasury Department, gives us his views on the market and why a number of metrics suggest a recession is increasingly likely.

A number of metrics suggest recession is increasingly likely…

……as central bankers tighten aggressively to flush inflation out of the system

In his semi-annual testimony Fed Chair Powell conceded that a soft landing will be very challenging…

…but with inflation yet to peak central banks will likely keep tightening aggressively in the near term

Conditions for a recession sliding into place…

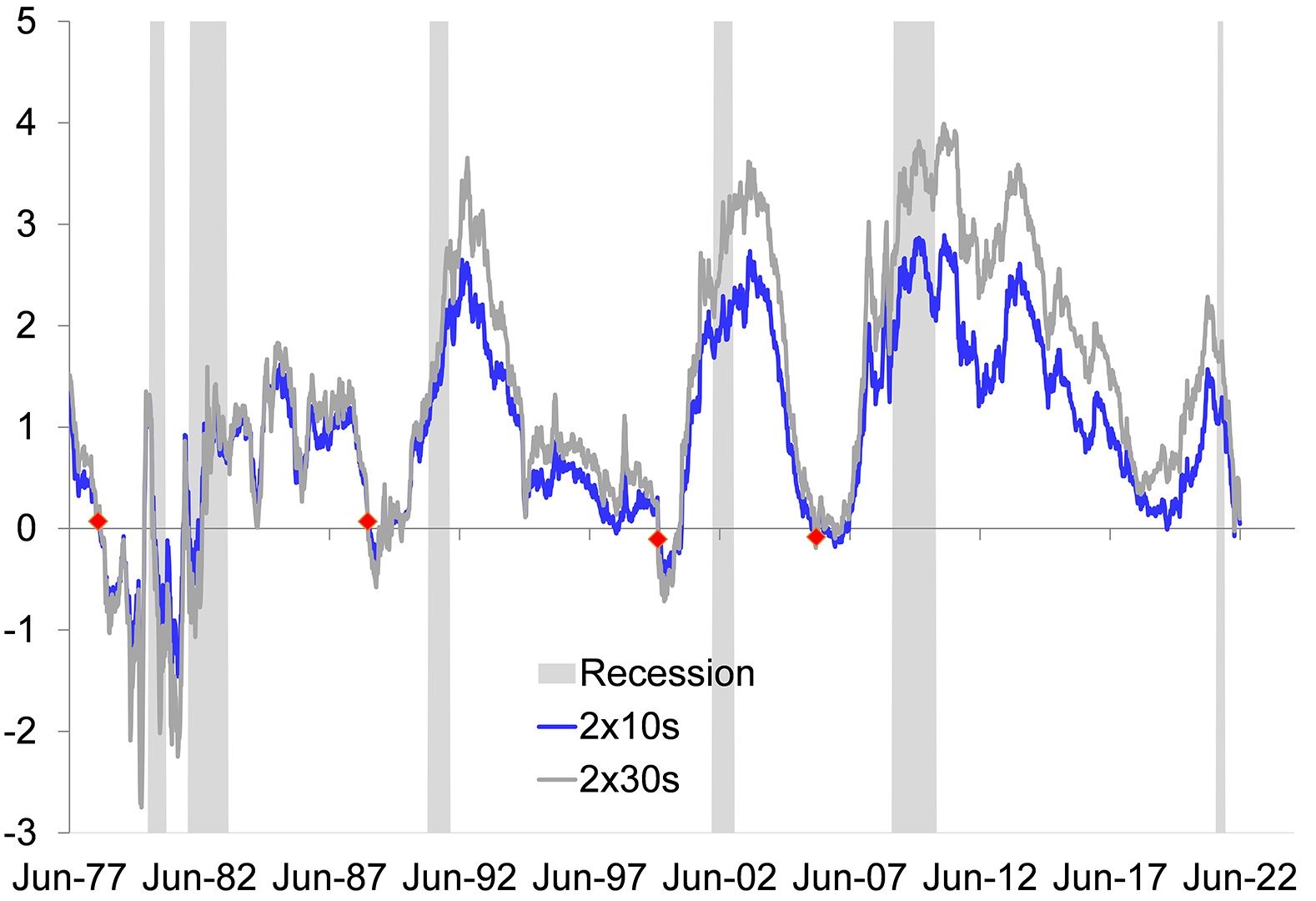

The 1979~87 Federal Reserve Chair Paul Volker is famous for removing the punch bowl and squeezing inflation out of the system. It came at a heavy cost in terms of lost output but it was arguably necessary. It was a key component in setting the backdrop for firm growth in the back half of the 1980s and through the 1990s. In recent weeks, recession calls have surged and US equity markets have dropped into bear market territory as inflation continues to surprise on the upside and central banks, not only in the US but elsewhere too have stepped up the pace of policy tightening and rhetoric. Equity bear markets are closely associated with recessions in the US. Of the 8 bear markets for US equities seen since 1970 (excluding the current bear market where the jury is still out), six have happened either just before or concurrently with a US recession. In a mid-2019 article for Project Syndicate, Anatole Kaletsky argued that post-war US recessions were generally caused by one of three things: 1) substantial monetary or fiscal tightening; 2) a financial crisis; or 3) some kind of massive external shock that significantly increased energy prices. Both 1 and 3 are undoubtedly present currently and 3 is exacerbated by food prices running sharply higher too. Food inflation is running around 40-year highs. Another classic recession indicator is the yield curve. The 3mx10yr UST spread is flashing a very different signal from the 2x10yr UST spread, which briefly inverted in early April and is still close to zero. Powell’s recent comments on rate hikes at his semi-annual testimony suggests it will not be long before the signals merge. Powell noted “Financial conditions have tightened and priced in a string of rate increases and that’s appropriate…We need to go ahead and have them”. The 3mx2yr spread will narrow sharply in coming months, especially if the Fed sticks to 75bp hikes, as seems likely at least for July. The NY Fed’s DSGE model updated in mid-June now sees a soft landing (growth staying positive over the next 10 quarters) as just a 10% probability, while the probability of recession is (at least 1 quarter in the next 10 where YoY growth dips below -1.0%) is around 80%.

…which looks required to get inflation down

The Fed’s Barkin recently noted that the Fed wants to tighten “as fast as you can without breaking anything”. There is debate about whether it is possible not to break anything and bring inflation down or whether the Fed has to bite the bullet and accept that higher unemployment/recession is the price required for lower inflation as Volker did. Certainly, the haste with which the Fed is moving increases the chances of an accident. Larry Summers is a key proponent of the view that recession is inevitable if inflation is to be brought under control. Looking at prior recessions, he argues that every time the Fed has tightened enough to meaningfully slow inflation, it has resulted in recession. He argues the soft landings of 1965, 1984 and 1994 bear little resemblance to the current situation given much lower inflation and higher unemployment as their starting points. In a recent commentary former Fed Vice Chair Bill Dudley noted “If you’re still holding out hope that the Federal Reserve will be able to engineer a soft landing in the US economy, abandon it. A recession is inevitable within the next 12 to 18 months”. He argues that current inflation makes the Fed strongly focused on prices, where expectations are in danger of becoming unanchored. He sees limited ability to take the unemployment side of the mandate into account in these conditions.

The 2x10s UST curve is flat indicating slow growth, while cost pressures are easing but only slowly

The 2x10s UST curve is flat indicating slow growth, while cost pressures are easing but only slowly | |

|  |

Source: Bloomberg | |

Commodity prices rolling over, where supply is not constrained

Other indicators suggest global demand is slowing too. Copper is sometimes referred to as Dr Copper as it is widely used across the economy and is viewed as a proxy for global demand. Copper prices were down 20% in the second quarter having climbed around 5% in Q1. It is not just copper prices that were lower. Industrial metals fell down 10~30% in the second quarter. The Commodity Research Bureau publishes an index of raw materials (RIND) that are not traded on futures markets. It is down just over 10% from its early Q2 peak and has dropped below its 200-day moving average. It would be helpful if oil and gas prices were also dropping but both are supply constrained keeping them elevated, which in turn is both weighing on consumption and at the same time pushing the peak for inflation both higher and later. This is making the job of central banks significantly harder. Recent research published in the BIS annual report warns that many developed markets are at risk of sliding into a high inflation environment as services prices make up an increasing contribution to inflation and that central banks should focus on getting inflation under control. Service prices are more generally driven by wages and are traditionally stickier than goods price inflation.

Inflation to remain elevated in the near term

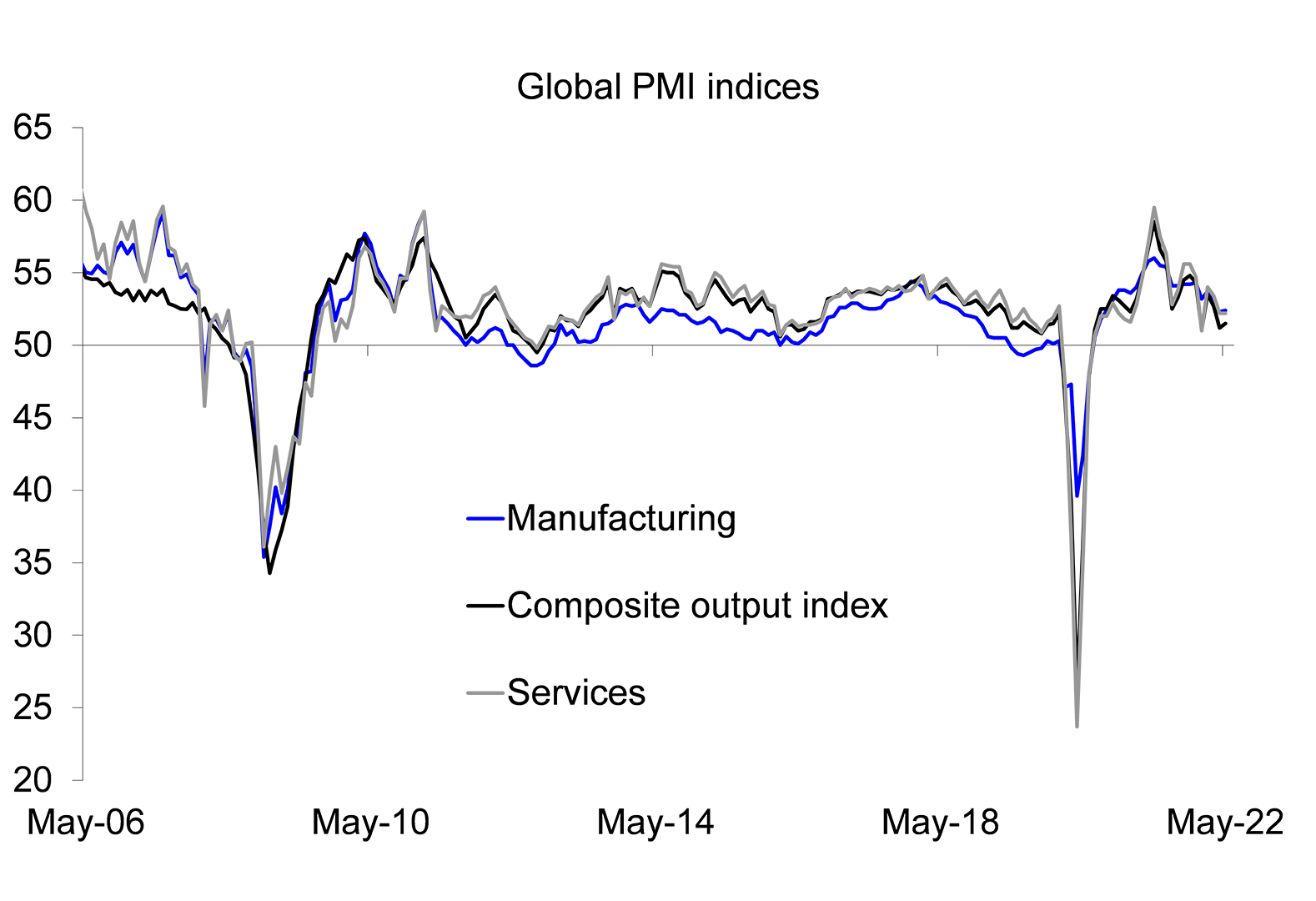

The message from the recent flash PMI surveys for June is that supply chain strains are easing but alas only very gradually. This should help lower prices for industrial goods but it looks as if such has been the economic momentum that pressures from the service sector will substitute for rises in industrial good prices in coming quarters and slow the decline in inflation. This leaves an unpromising backdrop for central banks. Inflation is sufficiently elevated that it remains the key focus even as the signs of the impending slowdown build. In recent cycles the prospect of weaker demand would lead to a rapid slowdown in tightening plans by central banks. This time round, such an abrupt stop is not possible given the inflation outlook. Rates are likely to remain high in the short run. Even in a recessionary scenario, it will hard to cut rates until there is clear evidence that inflation is set to undershoot target.

Difficult times for central banks as evidence of weaker growth is emerging faster than evidence of slowing inflation

The more elevated inflation outlook makes for difficult times for central banks. In general central banks are mainly concerned with the demand side of the economy as the supply side is slow moving and not especially responsive to monetary policy. Central banks are trying to align demand with existing supply over an 18~36m horizon over which changes in interest rates impact the economy. However, in the wake of the Covid crisis, the supply side of the global economy has been has been significantly more volatile than usual, which complicates the issue for central banks. The failure of participation rates to normalise has led to very tight labour markets, which are an increasing source of inflationary pressure in a way they haven’t been for many years. The growth outlook is weak enough to slow the pace of tightening in normal times but the current backdrop is anything but normal. With inflation yet to peak, it is likely that central banks will talk and probably act tough even as the outlook darkens. In his semi-annual testimony Chair Powell noted the commitment to the fight against inflation was “unconditional”. This should keep financial conditions tightening and asset markets under pressure. We see weak asset markets as a solid backdrop for the US dollar in the short run but expect that once inflation has more clearly peaked, the greenback will give back some of its recent gains.

PMI to slow further in June with the 50 level looming, keeping policy outlook and asset markets | |

|  |

Source: Bloomberg | |

See more Insights & Research from Mizuho