Message from the Group CEO

Setting the stage for our next challenge

Our society is one where multiple issues are intricately intertwined. What role should we at Mizuho play in such a society? What kind of society do we hope to create for the future? These are questions that we discussed in depth when formulating our current medium-term business plan, which we launched in fiscal 2023.

As customers confront the various challenges of today, we want to be by their side. We want to take on various challenges for ourselves as well. In doing so, we want to act as a bridge that connects our customers' endeavors and provides a platform for resolving the issues they are facing. Our determination to execute in these areas became the foundation for establishing our new corporate Purpose in 2023: "Proactively innovate together with our clients for a prosperous and sustainable future." The word "together" sums up what Mizuho aspires to do. In the last two years, I have been extremely pleased to confirm that this Purpose was indeed the right one for us.

Two examples epitomize our Purpose. The first is our value co-creation investment, in which we take business risks together with our corporate clients through direct equity participation in new businesses that seek to create new industries and markets. The second is our Mizuho NISA Cafes, where retail customers can freely join in consultations and seminars outside of regular branch operating hours, an idea that was originated by a branch employee and has since expanded nationwide. Each of these embody our Purpose by working together with our customers and society to address their needs.

We have carried forward our corporate DNA from the times of Eiichi Shibusawa, Zenjiro Yasuda, and Toyotaro Yuki, who were capitalists and entrepreneurs of Japan in the late 19th and early 20th centuries. These figures were instrumental to both the modernization of Japan and the development of Mizuho. They actively engaged with people in a spirit of co-creation, which remains at the core of Mizuho's identity. Looking closely at this corporate DNA, we have reaffirmed the need to realize societal value and not just economic value. Accordingly, we have defined our long-term goal for the future as personal well-being and a sustainable society and economy, and towards this goal we have set four 10-year milestones. The first milestone is progress toward a more inclusive society, in which everyone is able to lead a healthy and happy life; the second is widespread adoption of innovative technology such as AI, which will improve convenience and productivity; the third is reversing Japan's decline and putting the Japanese economy on a growth trajectory; and the fourth is accelerating the move toward global sustainability, which will lead to coexistence and mutual prosperity, as advocated by Shibusawa.

To realize our vision for the world 10 years from now, in fiscal 2023 we identified five business focus areas: (1) improving customer experience, (2) asset and wealth management in Japan, (3) enhancing the competitiveness of Japanese companies, (4) global Corporate & Investment Banking (CIB) business, and (5) sustainability and innovation. The recent implementation of US tariff policies has heightened uncertainty in global affairs. A major paradigm shift is taking place amid the advancement of globalization. What does this shift indicate? I believe it means that each country needs to recognize its own strengths and challenges and forge its own path to success. Now more than ever, Japan must lay down such a path to tackle its myriad challenges, including labor shortages stemming from the declining birthrate and aging population, low self-sufficiency in food and energy, and diminishing global competitiveness among local industries. I am confident that our five business focus areas, which comprise the core of our strategy, are in line with the needs of the era. (1) to (3) will strengthen the competitiveness of Japan. In this regard, while there may be some conflicting interests at the level of national governments, collaboration within the private sector is still a priority. (4) will promote global collaboration through cross-regional cooperation, and (5) will extend commitments to sustainability. We will remain steadfast in moving forward these business focus areas.

In fiscal 2024, we achieved the financial targets of our medium-term business plan one year ahead of schedule. Subsequently, in fiscal 2025, we have introduced new medium-term financial targets. Because the business environment has been changing at a rapid pace in recent years, rather than making a set timeline of three years for achieving our medium-term financial targets, we will revise them flexibly in line with the changing business environment. This will serve to ensure highly transparent communication with our stakeholders.

Progress of the target business model

In this section, I will discuss the progress and challenges in our five business focus areas and the status of the corporate culture transformation we have been pursuing since I assumed my role as Group CEO. I will also explain the challenges we must address as a company to achieve further growth.

Progress and challenges in the five business focus areas

(1) Improving customer experience (mass-market retail business in Japan)

In Japan, over the past few years, we have been working to improve our online banking app and website Mizuho Direct. Through these efforts, our active users have increased 60% compared to fiscal 2022. In addition, account openings have trended upward, due mainly to various promotions and the launch of the Mizuho Rakuten Card credit card, in partnership with Rakuten Card. The key to maintaining a competitive edge over other companies will be in developing more effective promotional campaigns and redesigning our approaches from a user-oriented perspective. I have come to realize this past year that we may learn much in this area from Rakuten's expertise in digital technology. Also, in March 2025 we entered into a capital and business alliance with beBit, Inc., a leading company in user experience (UX) consulting services. We will leverage this alliance to further improve customer experience.

Improvements have also been made to our contact centers and branches. In August 2024, we introduced AI at our contact centers to facilitate more timely responses to customer inquiries and concerns. This has reduced our response time per case, enabling us to respond more quickly. As it is an ongoing process, we will continuously work to improve in this area.

Meanwhile, our branches increasingly cater to customers who prefer the experience of direct, in-person engagement. We will do our utmost to improve customer experience through services offered at our branches, contact centers, and through Mizuho Direct.

(2) Asset and wealth management in Japan

In Japan, awareness of asset and wealth management is increasing each year, with the encouragement of the Japanese government, among other factors. However, many customers still find it a major challenge to become actively involved in asset building. To better serve them, we introduced NISA Cafes, where customers can consult with us about Japan's Nippon Individual Savings Account (NISA) tax-exempt investment scheme, at our branches throughout Japan. We have since come to stand out among Japan's three largest banks in terms of NISA account openings, and including Rakuten Securities, in which we own a 49% stake, we are one of the leading financial institutions in Japan in terms of the number of NISA accounts. That said, we must continue to refine our wealth management business and turn it into a source of differentiation. Our investment in Rakuten Securities has enabled us to reach all customer segments, from individuals starting out in asset management to high-net-worth investors, and engage with customers both in person and online. Going forward, we will provide consulting services that cater specifically to the goals of each customer by systematically training and developing relationship managers, who meet face-to-face with customers, and by expanding our product lineup. As part of our product development, we acquired a minority stake in Golub Capital in the US, through which we obtained exclusive rights to sell Golub Capital's products in Japan. This will allow us to capture the widespread interest in private credit among institutional investors and high-net-worth investors. We will continue to expand our product lineup to include private asset investments, such as infrastructure and real estate.

(3) Enhancing the competitiveness of Japanese companies

Mizuho has traditionally been strong when it comes to business with Japanese companies, able to apply our extensive track record in industry research, as well as our experience and expertise in consulting on the future of industries and in business and industry restructuring. These are major advantages in terms of transforming industry structures and developing a sustainable society. We have begun deploying the strengths of our industry research to middle-market firms and are actively discussing business development and sustainability with their respective CEOs and CFOs. Revenues from corporate solutions for middle-market firms have steadily increased as a result. We have also been supporting business succession and startups / innovative companies. Client needs for business succession continue to diversify. Mizuho Bank, Mizuho Trust & Banking, and Mizuho Securities are working together to provide concerned business owners with one-stop solutions for transferring their business and assets smoothly to the next generation. As for supporting startups / innovative companies, we have focused particularly on the task of providing risk capital to the deep tech field. Because of this, our loan balance has increased 1.7-fold from fiscal 2022.

With fierce competition from China and other countries, it is essential that Japanese industries find a path forward. The development of industries, from small and medium-sized enterprises (SMEs) to large corporations, is the root of Japan's national competitiveness, and we will continue to play a key role in this effort. To that end, we recognize the need to enhance productivity using limited resources and to further strengthen our resource allocation capabilities for SMEs. I am convinced Mizuho is in a position to fully demonstrate our raison d'être.

(4) Global Corporate & Investment Banking business

We have honed our strengths in the global Corporate & Investment Banking (CIB) business, particularly in the US. In 2015, we purchased North America assets from Royal Bank of Scotland (RBS), upon which just over 100 coverage bankers and other professionals became members of the Mizuho group. We have since developed our debt capital market (DCM), equity capital market (ECM), and derivatives capabilities. Based on client needs, we have also developed our sales and trading (S&T) business, which underpins the growth of our primary business. Accordingly, our gross profits in the Americas have grown 20% compared to fiscal 2022. In fiscal 2023, we made US-based M&A advisory firm Greenhill a wholly owned subsidiary. Through this acquisition, we have furthered our M&A and equity capabilities, and our investment banking platform is now on the verge of completion.

Our CIB business has steadily increased our presence in the US market and we have seen drastic growth in the number of job applications. This has created a virtuous cycle in which the acquisition of exceptional talent leads to the stable and continuous growth of business. With Greenhill at the center, we will strive for further growth by strengthening cross-regional collaboration between Japan, APAC, EMEA, and the Americas, which has already been showing positive results. There has been a considerable increase in collaboration between bankers in Japan and the Americas, as well as a growing number of cross-border M&As between Japan and the US. In addition, during our current medium-term business plan, our global CIB business has been working to reduce low-profit assets.

(5) Sustainability and innovation

Sustainability involves both risks and opportunities. In this section, I will discuss the sustainability of our business. For other aspects of sustainability, please refer to our various reports and releases from May to July 2025.

While we set our sustainable finance target for JPY100 trillion by fiscal 2030, we have steadily accumulated JPY 40.3 trillion in sustainable finance as of the end of fiscal 2024. In the process, we have introduced or helped design various new financing methods in cooperation with business partners, such as GHG Visualization Impact Finance to support SMEs, Sustainable Shipping Impact Finance to promote decarbonization in the maritime transportation sector, and a sustainable finance framework for the development of carbon neutral ports. We have identified hydrogen, carbon credits, impact, and circular economy as four areas to focus on from a sustainability perspective and made strides in each area. Amid ongoing changes in the international situation, sustainability remains a priority. Mizuho will continue to push forward in resolving societal issues and enhancing corporate value.

Corporate culture transformation as a catalyst for continuous growth

As Group CEO, I believe it is my duty to foster a sound corporate culture and develop strategies that allow Mizuho to demonstrate its strengths. A sound corporate culture inspires employees to be motivated and innovative. If we focus our strategies on areas where we can leverage our strengths, employees will experience success, be more motivated, and take on new challenges. The only way we will naturally continue to grow is by achieving a virtuous cycle of culture and strategy. I discussed our strategy in the previous section, and I will now explain briefly our corporate culture transformation.

The only way we will naturally continue to grow is by achieving a virtuous cycle of culture and strategy.

We aim to build a corporate culture that enables anyone to express their views in a constructive manner and that encourages everyone to pursue new initiatives and the development of innovative solutions through active discussion. By operating responsibly and transparently for all stakeholders, we will work together to achieve our vision for the world.

There are three key points to this. The first is defining a purpose to create a sense of unity among employees. Ours, as described earlier, is to "Proactively innovate together with our clients for a prosperous and sustainable future." The second point is establishing a human resources framework that cultivates individuals who will take initiative on their own and embrace new challenges. In Japan, we introduced our new human resources framework, CANADE, in fiscal 2024. This framework attaches greater importance to individual roles and achievements, as we break away from the traditional Japanese seniority system and promote capable individuals to advanced roles regardless of age. The third point is creating a corporate culture in which employees with a range of different backgrounds and experiences can thrive. This includes promoting highly competent employees regardless of gender and actively recruiting outside the organization.

In spearheading our corporate culture transformation, each year Group Chief Culture Officer (CCuO) Natsumi Akita and I visit over 100 offices and hold 15 to 20 town hall meetings at our Head Office, meeting and talking with employees.

Through these efforts, we have made solid progress in our corporate culture transformation. We promised to raise both our engagement score and inclusion score to 65% by the end of fiscal 2025, and we have nearly achieved this goal a year ahead of schedule. Even so, corporate culture transformation is an ongoing process, and one we will continuously work to advance.

Group-wide challenges to overcome for sustainable growth

So far, I have discussed the progress and challenges in our five business focus areas and corporate culture transformation. The business environment is expected to remain highly uncertain and volatile. Due to the decrease in Japan's working population, stemming from the declining birthrate and aging population, we will need to change our business model to incorporate the use of technology even further. Consequently, it is imperative Mizuho continues to become a more lean and resilient organization that boldly embraces challenges with an eye on the future and reinforces the catalysts of business growth. From these perspectives, we must resolve the following issues as quickly as possible.

(1) Streamlining and optimization of organizational structure

More complex organizational structures lead to fewer opportunities for dialogue and higher management costs at each level. We have been looking into streamlining Mizuho Trust & Banking's organizational structure and integrating Mizuho Bank and Mizuho Research & Technologies, and we will continue to explore possibilities for consolidating and reorganizing our group companies and simplifying our business lines.

(2) Cost restructuring

Rapid inflation, wage increases in Japan, soaring vendor costs, underinvestment during the past capital accumulation phase, and regulatory compliance have all contributed to a significant increase in our cost base. These unavoidable events make it clear that streamlining our cost structure is essential to our sustainable growth. Accordingly, we will conduct an extensive review of our work processes and revise our products and services, as well as assess the feasibility of using third parties such as consultants and SaaS providers.

(3) Ensuring alignment of strategies with resource allocation

The declining working age population in Japan is sure to strain resources. We will decide on investments after rigorously assessing their alignment with our strategies and their expected returns. We will also further clarify our objectives, particularly in areas where we have struggled with operational stability and strategy execution, and based on this, we will allocate and train appropriate personnel.

(4) Use of AI

Though AI is becoming more commonplace throughout our organization, for the most part it is being used only as a means of revising work processes. We will review our conventional work processes from the bottom up, position AI as a source of differentiation, and embrace bold reform. At the same time, we will take measures to develop personnel who can use AI effectively on a day-to-day basis and thereby create new value.

With the commitment of Group Chief Strategy Officer (CSO) Naoshi Inomata, Group Chief Financial Officer (CFO) Takefumi Yonezawa, and all executive officers of the Mizuho Financial Group, we will take a comprehensive optimization approach to group-wide issues.

In conclusion: Creating an organization that respects different values

My goal is for Mizuho to transform from a Japanese financial institution with a global footprint to a global financial institution that embraces its Japanese heritage and bridges diverse cultures.

In April 2025, we appointed Suneel Bakhshi, current President & CEO of Mizuho International, our securities subsidiary in Europe, as a Deputy President & Executive Officer of Mizuho Financial Group. Despite building a global business foundation, until now Mizuho has never promoted a non-Japanese member to its management team. I believe attracting management with a wealth of experience in cutting-edge financial markets is evidence of our ability to compete on the global stage. With this appointment as a starting point and symbol of our ambition, we will move quickly to become an organization where our people who have built their careers outside Japan can harness their strengths in any of our departments and offices. We will be a financial institution where diverse talent play an active role throughout the organization, including management, and where our people can engage in global discussions in all aspects of our business.

My goal is for Mizuho to transform from a Japanese financial institution with a global footprint to a global financial institution that embraces its Japanese heritage and bridges diverse cultures.

We will maintain our virtuous cycle by strengthening our approach in the five business focus areas and working together with employees to transform our corporate culture. We will also set the stage for further growth by approaching group-wide issues with unwavering resolve. We look forward to your continued support.

Masahiro Kihara

Message from the Deputy President

.jpg)

It is my honor to be invited by President & Group CEO Masahiro Kihara to take on the role of Deputy President of Mizuho Financial Group. I will step full time into the role from October 1, which will follow seven rewarding years as President & CEO of Mizuho International, including the last several years as EMEA Head of the Corporate and Investment Bank.

My career has spanned more than 40 years and it has been a privilege over this time to have lived and worked in seven countries across all regions, putting me in the fortunate position of gaining a truly global perspective. In the five years I have lived in Japan, as well as the 30 plus years that I have worked for, and with Japanese organizations, I have developed a deep respect and appreciation for Japanese culture, values, and ways of doing business. I am now very much looking forward to bringing my experience and insights to this global role in Mizuho Financial Group, to advance our ambitions of becoming a truly global financial group, deeply rooted in the strength and heritage of Japan. It is from this strong base and leveraging our talent in all regions that I hope to extend our reach and relevance across the world.

Globalizing our business approach presents an exceptional opportunity to bring our diverse operations into a more cohesive and collaborative partnership with our clients, so that together we navigate an increasingly complex world. We believe that our path forward is clear; we must be yet more agile and responsive in creating and delivering solutions to our clients.

Mizuho's unique identity, nourished by our Japanese heritage, but equally responsive to the customs of the various countries and regions that we operate in, allows us to offer our services with precision and a long-term commitment; qualities that are ever increasingly valued by our clients and stakeholders.

Instilling a partnership-like mentality that holds the governance and operating models together is vital. I intend to work to ensure our high caliber talent, both specialist and generalist, has the global mindset to enjoy working in a cross-cultural, integrated team. This will be core to my new role as we seek to further deepen our client relationships. This requires additional effort at times, rather than working within our own regional cultures, but I strongly believe the rewards of harnessing the full strength of our globality, as one team, will always outweigh the effort.

I believe that strong leadership combined with incentivizing a global mindset will deliver true cross-regional partnering for the benefit of our clients and the communities in which we serve. This ability to partner globally at scale is not just a strength—it is the essential code to unlocking new opportunities in driving solutions for our clients and to meet our obligations towards our stakeholders.

I look forward to working alongside our leadership team to deliver the continued success of Mizuho Financial Group as we pursue our next phase of growth. Together, we will build a more global, more connected, and more client-centric Mizuho—one that honors our heritage while shaping a dynamic future.

Suneel Bakhshi

Message from the Group CFO

.jpg)

Looking back on the second year of the medium-term business plan

Since the Bank of Japan implemented its negative interest rate policy in 2016, we have strategically focused on strengthening profitability through diversification of our business portfolio, optimizing cost and capital efficiency with disciplined financial management, and reinforcing our capital adequacy to ensure our sustainable growth. In fiscal 2024, we truly began to see the tangible results of our efforts taking shape.

Looking back, fiscal 2024 was marked by historic events. In the US, the presidential election brought changes in the administration, while in Japan, the Bank of Japan initiated interest rate hikes, signaling the end of its negative interest rate policy and the beginning of a normalization of monetary policy after eight years. Meanwhile, financial institutions benefited from a favorable operating environment, underscoring the stability of broader market conditions, and active corporate investment also contributed to strong business growth.

With such an operating environment, we achieved steady business growth in both customer and market divisions. Fiscal 2024 saw record-high Consolidated Net Business Profits and Profit Attributable to Owners of Parent, while we maintained credit-related costs at low levels by proactively preparing provisioning with a forward-looking perspective. Consolidated ROE improved to 9.4%, greatly exceeding the target of over 8.0% that we had set for the final year of the current medium-term business plan, and we achieved all of the financial targets in said plan one year ahead of our initial schedule of fiscal 2025.

Moreover, we invested in Rakuten Securities and Rakuten Card and acquired Greenhill. We also carried out growth investments contributing to Mizuho's unique competitive edge and enhanced shareholder returns through our first share buyback in 16 years. We believe the share buyback was received positively by the capital markets and has provided momentum for the next stage of our management.

Progress on medium-term business plan targets (Figure 1)

.avif)

- Excluding Net Unrealized Gains (Losses) on Other Securities.

- Including Net Gains (Losses) related to ETFs and others.

Perspective on the economic and financial environment in fiscal 2025 and beyond

The second Trump administration, inaugurated in January 2025, has again pursued an "America First" agenda, aiming for private-sector-led economic growth and low inflation. Key policy initiatives include energy cost reductions, permanent income tax reductions, administrative and fiscal reforms to secure financial resources and curb long-term interest rates, and reciprocal tariffs to address trade imbalances and revive domestic manufacturing. These changes will have impacts across diplomacy, trade, and national security, and they are already having a considerable influence on the real economy and financial markets. In particular, if economic tension between the US and China escalates, there could be disruptions to the global supply chain and subsequent declines in economic growth rates. Also, concerns over diminished confidence in the US could destabilize credit markets, potentially leading to significant deterioration in the global economic and financial environment. Therefore, the outlook remains highly uncertain.

My role as CFO is to achieve stable profit growth even in the face of such a challenging business environment. In fiscal 2025, maintaining a robust balance sheet through flexible and disciplined financial management and responding to changes in the economic and financial environment will be even more crucial. At the same time, we will further strengthen our business portfolio through diversified and complementary revenue streams to minimize profit volatility.

New medium-term financial targets and fiscal 2025 targets

Having achieved all fiscal 2025 financial targets one year ahead of schedule, we have set new medium-term financial targets to achieve by fiscal 2027. Given the diverse scenarios that could unfold due to the Trump administration's economic and trade policies and the responses taken by China and other countries, we have outlined three potential paths: favorable conditions, gradual recovery, and stagnation. Based on these scenarios, we have set new targets for Consolidated Net Business Profits and Tokyo Stock Exchange (TSE) ROE. The assumed scenarios and new medium-term targets will be revised as appropriate. As indicated in Figure 2, we are targeting TSE ROE of over 10% and Consolidated Net Business Profits of approximately JPY 1.4 – 1.6 trillion.

To that end, in fiscal 2025, we aim for record-high Consolidated Net Business Profits of JPY 1.28 trillion, Profit Attributable to Owners of Parent of JPY 940.0 billion, and TSE ROE of approximately 9%. While Profit Attributable to Owners of Parent amounted to JPY 885.4 billion in fiscal 2024 after taking into account financial measures such as realizing losses from the foreign bond portfolio and proactive provisioning, we firmly believe that Mizuho has a strong earnings base that could generate JPY 1.0 trillion under normalized conditions, excluding extraordinary factors. Based on this figure and factoring in expected growth in Net Business Profits, we aim to increase Profit Attributable to Owners of Parent to JPY 1.05 trillion in fiscal 2025. However, considering potential negative impacts on Net Business Profits, credit-related costs, and net gains related to stocks, we have conservatively set our fiscal 2025 guidance at JPY 940.0 billion. We intend to revise this guidance as necessary, based on changes in our external business environment.

Setting new medium-term financial targets (Figure 2)

.avif)

- Including Net Gains (Losses) related to ETFs.

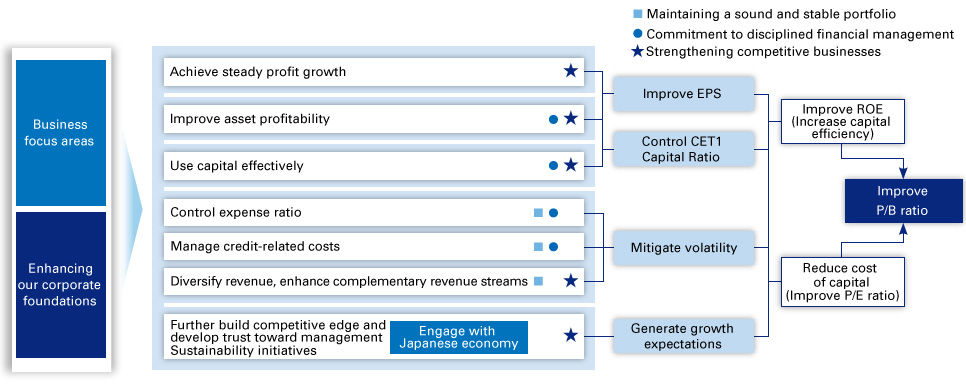

Progress of measures to improve the P/B ratio

Mizuho’s price-to-book (P/B) ratio has been improving, driven by increases in ROE and expectations for sustainable growth. However, compared to our global peers, there is still room for improvement, despite differences in policy interest rates across countries. Further improving our P/B ratio is a top management priority, and we will continue our efforts toward achieving this goal.

The path to an improved P/B ratio will be realized through increasing ROE and our price-to-earnings (P/E) ratio. As set forth in our medium-term financial targets, we aim to increase TSE ROE to over 10% by fiscal 2027, while solidifying Mizuho's unique competitive edge and enhancing the P/E ratio. To achieve this, we will maintain a sound and stable portfolio, committed to disciplined financial management. The business aspects of our approach are discussed in "Business model for value creation" on page 33, so here I will focus on the financial aspects.

P/B ratio comparison to global peers1 (Figure 3)

.jpg)

- Created by Mizuho based on Bloomberg data. Closing price as of April 30, 2025 used for P/B ratio.

To improve our P/B ratio, we will take the following four key financial measures: improve earnings per share (EPS), control the CET1 Capital Ratio, mitigate volatility, and generate growth expectations (see Figure 4). By continuing to firmly pursue our six initiatives, we will steadily produce results and gain trust from our shareholders and investors.

Approach to improving P/B ratio (Figure 4)

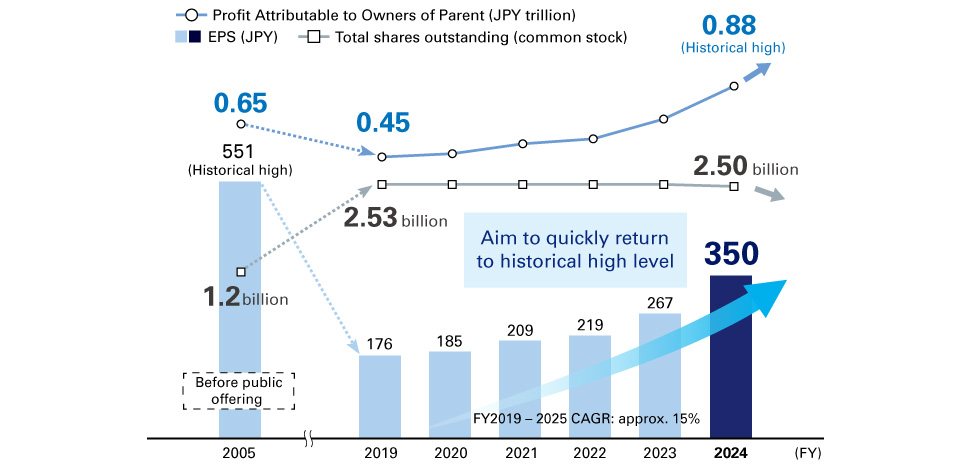

1. Achieve steady profit growth

In fiscal 2024, Consolidated Net Business Profits reached a record-high JPY 1,144.2 billion, an increase of approximately JPY 340.0 billion from fiscal 2022, and of which around JPY 200.0 billion was realized through strengthening our business focus areas.

We saw significant improvement in results particularly in our corporate business in Japan by providing tailored proposals and financial solutions to address the increasing corporate actions from large corporations and middle-market firms. Also, our global CIB business demonstrated strong performance, especially in the US, where we improved our position in the league tables.

In fiscal 2025, uncertainties over US policies may have a global impact by curbing investment and corporate actions, potentially leading to a decline in profits in the primary business of our corporate business in Japan and global CIB business. We will strive to increase profits in secondary business by capturing the opportunities that arise from increased demand for hedging of foreign exchange and interest rate risk, which stems from the expanding volatility of financial markets, as well as increased order flow from the asset reallocation decisions of institutional investors. We also expect higher demand for consultation and discussion from our corporate clients on strategy restructuring in response to major changes in the business environment. To address these needs, we will create business opportunities by leveraging Mizuho's strengths, such as the research capabilities of the Industry Research Department of Mizuho Bank and the advisory and consulting capabilities of Mizuho Trust & Banking and Mizuho Securities. Furthermore, in light of significantly volatile financial markets, we will strive to thoroughly respond to retail customers in accordance with our customer-oriented business conduct and build trusted relationships in the asset and wealth management business, which will lead to an increase in assets under management and growth in related revenue.

2. Improve asset profitability

To improve ROE, we will also continuously improve return on risk-weighted assets (RORA). In our clients' businesses, we will assess the profitability of all clients, transactions, and products, reallocating management resources to businesses with higher RORA. Specifically, we will reduce low-RORA segments such as housing loans subject to intense interest rate competition and long-standing customer loans that have shown limited RORA improvement. The management resources freed up as a result will be invested in high RORA businesses such as M&A-related finance, real estate finance, and other businesses with the potential to generate various ancillary revenue.

We also continue to work on reducing cross-shareholdings. The book value of our cross-shareholdings, which stood at approximately JPY 2.0 trillion at the beginning of fiscal 2015, has been reduced to approximately JPY 0.8 trillion over the past 10 years. Moving forward our plan of reducing the book value by JPY 300.0 billion over the three years from fiscal 2023, we have sold JPY 186.1 billion in cross-shareholdings as of the end of fiscal 2024. In recent years, our clients have become increasingly aware of the need to reduce cross-shareholdings due to growing demand for stronger corporate governance. Accordingly, we have drawn up a new plan to reduce the book value by JPY 350.0 billion or more over the three years from fiscal 2025 in order to accelerate reduction, while still intending to achieve our initial plan of reducing the book value by JPY 300.0 billion by fiscal 2025. In terms of deemed holdings of shares, we will proceed with measures to reduce these by JPY 200.0 billion over the three years from fiscal 2025. Based on our stock price at the end of March 2025, we aim to reduce the market value of cross-shareholdings, including deemed holdings of shares, to less than 20% of net assets within three years.

Risk-weighted assets (RWA) and RORA1 (Figure 5)

- RWAs calculated on a management accounting basis (figures for March 2025 preliminary). Includes interest rate risk in banking account. RORA: Gross Profit RORA. As of fiscal year-end.

3. Control expense ratio

Through disciplined cost management, Mizuho has maintained its expense ratio around 60% which is comparable to that of major European and US banks despite the large difference in policy interest rates. With the increasing uncertainty of our business environment and the heightening risks associated with its severity, we will reduce fixed costs to strengthen the downward resilience of earnings. Under the strong commitment of management, we will improve the efficiency and productivity of our business processes by dynamically scaling back products, services, and businesses in which we have less of a competitive advantage. At the same time, we will actively invest in the necessary areas to ensure stable business operations as a financial institution and reinforce our competitive edge.

4. Manage credit-related costs

Due to changing economic and trade policies, including the introduction of reciprocal tariffs in the US, the business environment will likely become more severe, especially in sectors that are highly dependent on exports to the US. We need to be aware of the possibility that our clients' financial conditions may deteriorate and credit-related costs may increase. Accordingly, in fiscal 2024, we proactively allocated JPY 92.4 billion for provisions targeting sectors expected to experience adverse effects, ensuring readiness for future risks. By closely monitoring customers’ business and financial conditions and offering restructuring and improvement proposals before difficulties arise, we will continuously work to control credit costs.

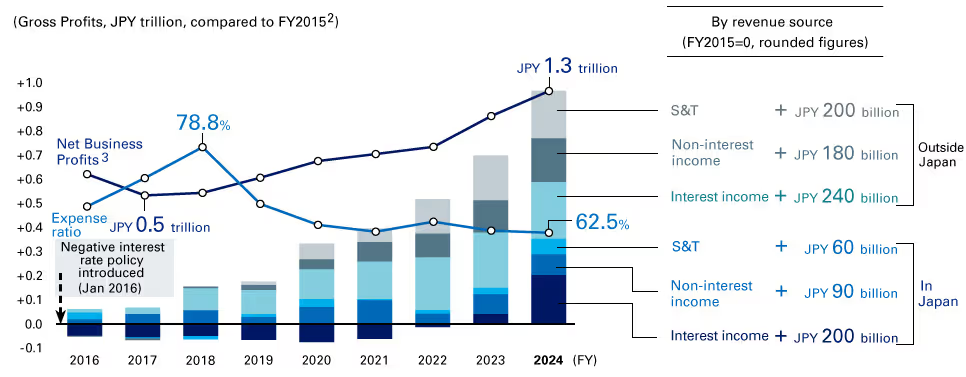

5. Diversify revenue and enhance complementary revenue streams

Having been faced with a difficult situation where interest income in Japan was significantly reduced due to the Bank of Japan's negative interest rate policy, we have diversified our business portfolio in and outside Japan, expanded non-interest income, and achieved earnings stability and growth. Particularly, we have achieved strong earnings growth for the global CIB business centered on the US by pursuing synergies between commercial banking, investment banking, and sales and trading (S&T) businesses with highly credit-worthy blue-chip companies and institutional investors as main clients. Compared to other peers in Europe and the US, Mizuho's global CIB business model is characterized by a low percentage of trading revenue, which fluctuates greatly in response to financial market conditions. Because of that low percentage, our global CIB business model produces extremely stable earnings.

The Japanese economy continues to gradually achieve nominal growth, and since the negative interest rate policy was lifted in March 2024 policy rates have remained positive. As a result, interest income in Japan will likely continue to increase. However, we remain prepared in case of any potential declines in policy rates, which could significantly impact deposit and loan profitability in customer divisions. We are flexibly controlling our Japanese yen and foreign currency bond portfolio in markets divisions while anticipating this possibility. This approach will mitigate fluctuations in our overall revenue from changes in policy interest rates and ensure that the revenue streams from our customer and markets divisions complement one another to an even greater extent.

Breakdown of revenue1 and expense ratio (Figure 6)

- Customer divisions + S&T

- For S&T, FY2016 – 2018: compared to FY2015, total of in and outside Japan.

FY2019 – 2024: compared to FY2018. - Consolidated, including Net Gains (Losses) related to ETFs and others. Excluding the realization of losses in securities portfolio.

6. Use capital effectively

We will maintain our capital management policy of achieving an optimal balance between capital adequacy, growth investments, and enhancement of shareholder returns. While capital adequacy has long been a financial challenge for Mizuho, we have retained approximately half or JPY 2.7 trillion of the JPY 5.5 trillion in Profit Attributable to Owners of Parent recorded over the past 10 years as capital. As a result, our CET1 Capital Ratio (excluding Net Unrealized Gains (Losses) on Other Securities), a regulatory ratio, improved significantly and has reached a sufficient level of 10.3%, close to the upper limit of the operation range. In light of this, we will place greater emphasis on allocating future Profit Attributable to Owners of Parent to enhancing shareholder returns and making strategic growth investments.

Historical level of CET1 Capital Ratio and allocation of Profit Attributable to Owners of Parent (Figure 7)

- Basel III finalization fully effective basis. Excluding Net Unrealized Gains (Losses) on Other Securities. As of fiscal year-end.

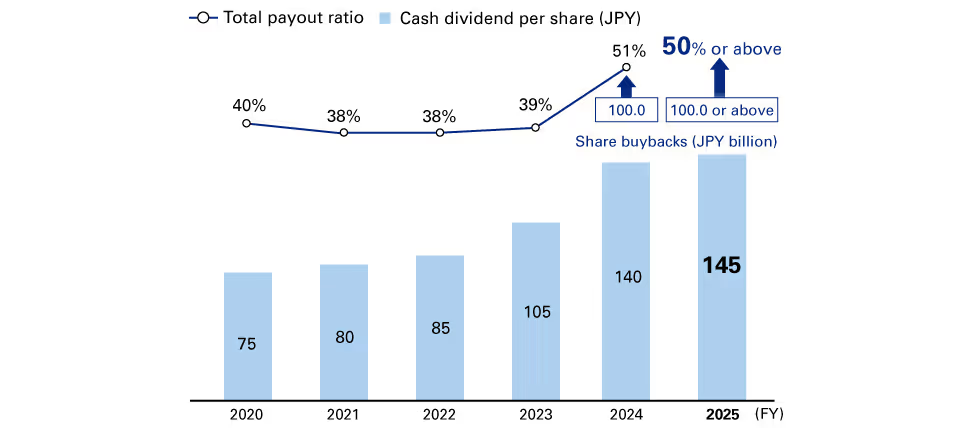

Given these gradual changes in our capital policy, we revised our shareholder return policy, which now calls for progressive increases in dividends per share and the execution of flexible and intermittent share buybacks. In accordance with this new policy, we will increase dividends per share by approximately JPY 5 each fiscal year based on the steady growth of our stable earnings base and decide on share buybacks based on business results, capital adequacy, our stock price, and opportunities for growth investment, using a total payout ratio of 50% or more as a guide.

The key principles underlining this approach are as follows: (1) the scale of shareholder returns, a combination of dividends and share buybacks, should be indicated as the total payout ratio, given that it is now possible to continuously repurchase shares; (2) dividends, which are the basis of shareholder returns, should be steadily increased even in the face of downward pressure on earnings from the increasingly uncertain business environment and rapidly changing macro-environment; and (3) management's intention to steadily increase EPS should be demonstrated by reducing the number of outstanding shares through flexible share buybacks.

Improve EPS (Figure 8)

Based on our new shareholder return policy, we have established our shareholder return forecast for fiscal 2025: cash dividend per share of JPY 145 (a JPY 5 increase from fiscal 2024 and the fifth consecutive year of increases) and share buybacks of JPY 100.0 billion. Accordingly, the total payout ratio is expected to be approximately 50% based on our Profit Attributable to Owners of Parent forecast of JPY 940.0 billion, which will be revised as necessary. We will also consider further shareholder returns based on our capital adequacy ratio, stock price, and growth investment opportunities.

Shareholder returns and fiscal 2025 forecast (Figure 9)

Our approach to growth investment will also remain unchanged. We will determine growth investments in a careful and disciplined manner by conducting multifaceted and in-depth examination of consistency with Mizuho's strategies, adequacy of investment returns, effectiveness of governance, and compatibility of corporate cultures.

Since fiscal 2023, we have acquired Greenhill to strengthen our global M&A advisory function in our global CIB business and corporate business in Japan, and we have strategically invested in Rakuten Card and Rakuten Securities, both of which belong to the Rakuten Group, one of Japan's leading e-commerce platform companies, to strengthen the mass-market retail and asset and wealth management businesses. In the mass-market retail business in Southeast Asia, where there is potential for future growth, we are making limited amounts of experimental investments to accumulate knowledge from a fintech and digital finance point of view on the business and competitive environment and the penetration of new digital services, as well as to consider our next growth strategy. We will continue to make growth investments by carefully selecting and exploring investment opportunities that will strengthen Mizuho's unique competitive edge.

In making growth investments, we work closely with investee companies, drive business to realize the strategic intent of our strategy, monitor the progress of profit plans, and promote organizational integration through personnel exchanges and the strengthening of governance so that we can quickly realize the benefits of these investments. We will manage experimental investments in particular with discipline and will quickly exit if it is deemed that expected returns will not be realized.

To our investors

During a business trip to Europe at the end of 2024, I had the opportunity to sit down with an institutional investor who has made significant investments in Mizuho. I explained how we have reinforced profitability by diversifying our business portfolio, improved cost and capital efficiency through disciplined financial management, and enhanced our capital adequacy, especially during the challenging business environment following the negative interest rate policy. One remark stood out to me: "We are satisfied with the financial results achieved through your disciplined management. However, investors' expectations lie beyond your current trajectory. We would like to see Mizuho transform from a Japanese financial institution that operates globally to a truly global financial institution rooted in Japan." Together with our management team, we are committed to driving Mizuho forward into its next stage of growth.

We sincerely appreciate and welcome your candid feedback and continued support in the future.

Takefumi Yonezawa

Message from the Chairperson of the Board of Directors

.avif)

My commitment as Chairperson of the Board of Directors

In June 2025, four years after becoming an outside director of Mizuho Financial Group, I was appointed Chairperson of the Board of Directors. Over the course of my time as an outside director, I have engaged in supervisory activities both as chairperson of the Audit Committee and as a member of other committees. However, my new role as Chairperson of the Board carries special weight. Having taken up the baton from my predecessor Izumi Kobayashi, I am determined to chair the Board of Directors with a view to enhancing Mizuho's corporate value. I will here discuss my supervisory activities to date, review Mizuho's fiscal 2024 activities, and explain my approach to leading discussion at the Board of Directors for the achievement of the medium- to long-term growth strategy.

Supervisory activities to date and review of fiscal 2024

I became an outside director amid the turmoil of the IT system failures that persisted in Japan throughout 2021, and from my position as an outside director I witnessed the growing concerns among employees. At the time, I felt Mizuho's biggest challenge was the gap that existed between the holding company and entities, between each in-house company, and between management and supervision. To eliminate these discrepancies and connect and align all employees in the same direction, I advised that Mizuho needed to reflect on its history, from where it began to where it is now; rethink its raison d'être in society; and redefine its Corporate Identity and Purpose as a step toward transforming its corporate culture. Only then would it be able to effectively formulate a new medium-term business plan. The Board of Directors took up all of these points at our meetings.

Transforming corporate culture is not something that can be done overnight; it is, I believe, an ongoing task. The management team, including Group CEO Masahiro Kihara, has been working to transform Mizuho's corporate culture through the clear communication of Mizuho's Corporate Identity and Purpose to employees, and the positive outcomes of their efforts are quite evident when I talk to employees face-to-face in my visits to offices.

Mizuho's corporate culture transformation has been a major topic of discussion at the Board of Directors meetings and has continued to move forward, with various results also starting to show on the business side. In fiscal 2024, Mizuho posted record profits and achieved the financial targets of its current medium-term business plan, which began in fiscal 2023 and will still run through fiscal 2025, one year ahead of schedule. Considering that Mizuho also completed its first share buyback in 16 years, entered a strategic capital and business alliance with Rakuten Card and forged ahead on its post-merger integration with Greenhill, I would say that, overall, it was a year of significant progress.

The stance of the Board of Directors toward the achievement of the medium- to long-term growth strategy

While the financial targets of the current medium-term business plan have already been met, the duty of the chairperson remains the same as before: to lead the discussions of the Board of Directors and support the executive management team as it continues achieving its goals. Mizuho holds a competitive edge due to its expertise and track record in supporting industry development and corporate growth, in which it can utilize its relationships with various industries and its industry knowledge, as well as due to its global Corporate & Investment Banking (CIB) business model centered on the US. Further, it is improving customer experience across digital, remote, and physical channels in its retail business in Japan and establishing a framework for serving all customer segments, from individuals starting out in asset management to high-net-worth investors. At the Board of Directors, we will thoroughly explore the ways Mizuho can leverage its strengths and initiatives to refine the five business focus areas and turn them into a unique competitive advantage.

It is also important to enhance the corporate foundations underpinning Mizuho's business growth, which requires continuous corporate culture transformation, IT reforms, and maintenance of stable business operations. Mizuho, as a financial institution, has a role to uphold in providing social infrastructure, such as through its settlement and financial intermediary functions. I will chair the Board of Directors with a sharp focus on Mizuho continuing to fulfill this role under even the most difficult circumstances.