A Quarter of Records But NOT a Record Quarter

The first quarter of 2020 saw unprecedented dislocation of markets as the COVID-19 pandemic spread across the globe. Historic new records were set repeatedly – just not the kind of records anyone hopes for:

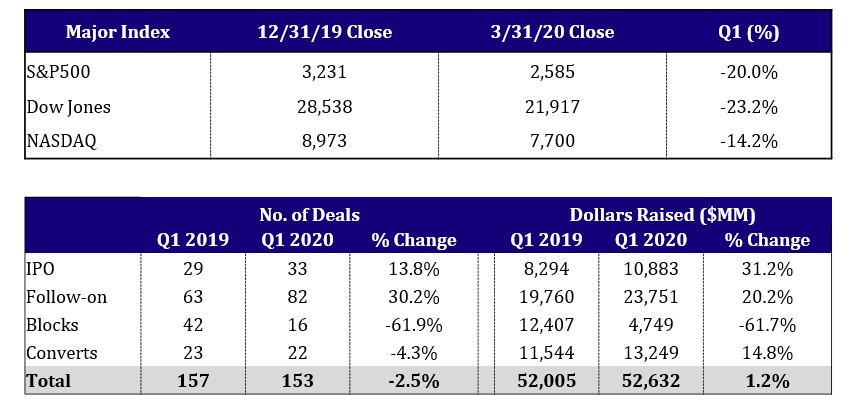

- The S&P 500 (-20%) posted its worst quarter since the 2008 financial crisis and the DJIA (-23%) posted its worst quarter in over three decades.

- March 2020 was a record-setting month with the top six largest point gains for the DJIA and fourth largest percentage gain (11.37%) in history. During the same month, the DIJA also saw the top six largest point declines and the second worst percentage drop (-12.93%) in history.

- The Volatility Index (VIX) hit an all-time high of 82 on March 16 after staying in the early teens for most of 2019 and early 2020.

- The yield on the U.S. 10-year Treasury also touched an all-time low of 0.318% in overnight trading on March 8.

- WTI Crude fell 66% in Q1 to $20.48 per barrel—the biggest quarterly decline currently on record.

- Overall equity new issuance was up slightly year-over-year for the quarter with 153 deals raising $52.6 billion in Q1 2020, compared with 157 deals raising $52.0 billion in Q1 2019. Considering that the new issue window was closed for much of Q1 2019 due to the government shutdown, this comparison is less than reassuring.

- Special Purpose Acquisition Companies (SPACs) continued to dominate the IPO market in Q1 with 13 deals priced to raise $3.7 billion. This represented 39% of all IPOs by number of deals and 34% by IPO proceeds raised. The average IPO performance for Q1 (ex-SPACs) was -1.3%.

Our Highlights as a Firm

Mizuho Equity Capital Markets participated in 13 equity deals as a Bookrunner or Co-Manager in Q1 2020 raising over $7 billion for clients, including Live Nation’s $400 million convertible notes offering and a $1.6 billion IPO for the drug research and biotech company PPD. Mizuho currently has mandates on seven TMT-related equity offerings totaling in excess of $2.5 billion.

Spotlight on TMT

TMT issuers raised $7.03 billion in the first quarter of 2020, accounting for ~13.4% of total issuance across all sectors. With equity markets declining 20%-30% during Q1, valuations have seen a commensurate decline. Most of the Global Diversified TMT names trade at a mean of 10x CY20 EV/EBITDA. High growth names (YoY Rev growth of 25%+) trade at a mean 9.2x CY21 EV/Rev. Many still trade in the teens though now only one is north of 20x (on either a CY20 or CY21 basis).

The software industry represented 65% of total TMT issuance in Q1 2020 with $3.2 billion raised and SPACs remained prominent in the TMT sector. Social Capital Hedosophia II and III (led by former Facebook executive, Chamath Palihapitiya) are on file to raise $900 million and there are currently an additional ~$1 billion of TMT SPACs in various stages of formation.

Convertible Market Commentary

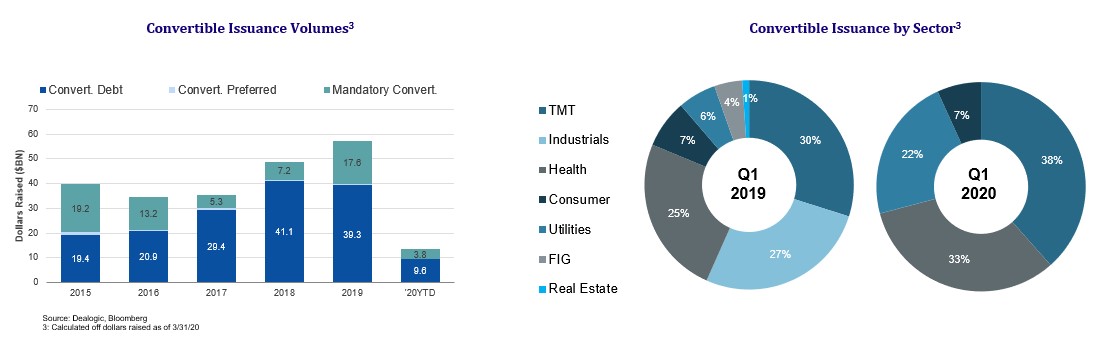

2019 was a banner year for convertible bonds and was dominated by issuers in the TMT space. 2020 was setting-up to be similarly attractive as coupons routinely touched 0% and conversion premiums hit 50%. This includes RingCentral (0.0% up 50.0%), Square (0.125% up 50.0%), and EnPhase Energy (0.25% up 52.5%). Terms were extremely attractive coming into the year. There were nine convertibles issued in Q1 2020 by TMT companies and median terms were 0.75% coupon, up 37.5% on a 5-year note. Two thirds of all TMT issuers utilized an additional derivative structure to bring the conversion premium up to either 75% or 100%.

We expect the convertible market to be one of the first to re-open. Investors remain hungry for product while volatility remains high and interest rates are at extreme lows. Slack’s $750 million convertible priced at 0.50% coupon, up 27.5% on April 6th shows clear evidence of this persistent enthusiasm.

Catalysts for Thought

COVID-19: The coronavirus pandemic is the proverbial “elephant in the room” when discussing this quarter’s economic outlook. The full impact of this global crisis, from both an epidemiological and markets perspective, is still unknown. Populations around the world wrestle with “stay at home” orders and “social distancing” mandates, while governments try to reconcile the human and economic cost of the pandemic. Only with hindsight will we be able to understand the long-term implications and how those will impact future equity market performance.

2020 Election: We were already in uncharted territory as we entered 2020 with an impeached president seeking re-election. The nation focused on the Democratic primaries as the pool of candidates narrowed to reveal a likely Joe Biden nomination. That clarity was short-lived, however, with many primaries postponed due to COVID-19 and pundits left to wonder how the election in November will be handled in its wake.

Profitable Growth: The equity market swoon has resulted in organizations with the riskiest business plans becoming most vulnerable. Continuing a theme that developed in late 2019, investors and analysts are skeptical of hyper-growth at all costs. WeWork remains the poster-child for this type of irresponsible growth strategy. The reversal in fortune (and investor sentiment) has been remarkably swift for WeWork and others like it.

Direct Listing: This hot-button subject of debate has quickly gone from topic du jour to barely discussed. Many companies that were rumored to be planning a direct listing are now reportedly pursuing more traditional IPOs. The direct listing still doesn’t permit the raising of primary capital, and in light of the recent market conditions, it’s understandable why raising more capital for the balance sheet would be so appealing.

.avif)