Overall Equity Capital Markets Commentary

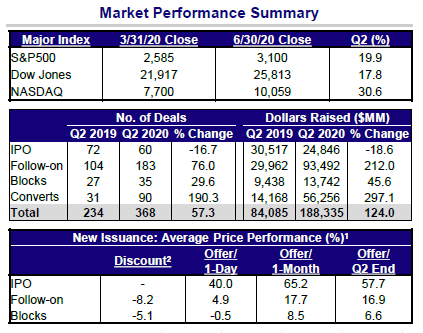

- Equity capital markets saw a stunning turnaround in Q2 2020 as the DOW, S&P500 and Nasdaq rallied 39%, 39% and 47%, respectively, from their March 23, 2020 lows.

- Equity new issuance volumes expanded dramatically in the second quarter. Some companies (airlines, cruise lines) sought to shore up balance sheets dented by the pandemic while others took advantage of new market demands brought about by the work from home WFH environment (security software, video conferencing, tele-health) and the intense focus on the healthcare sector (biotech/life sciences):

- Q2 saw total equity issuance of $188 billion which brought the YTD total as of 6/30/2020 to ~$241 billion. That amount equals ~93% of issuance for all of 2019.

- Overall, Q2 equity issuance was up 124% compared to the same period last year.

- The follow-on and convertible markets saw ~200% and ~300% increases YOY, respectively, making them the clear outperformers in terms of new issuance.

- After peaking at 83 on March 16 the Volatility Index (VIX) began a slow but steady retreat, closing out Q2 at 30.

- 24 Special Purpose Acquisition Companies (SPACs) priced in Q2 to raise $7.9 billion. This marked a record quarter in terms of proceeds raised. YTD, 37 SPACs have raised $11.7 billion, just shy of the all-time high of SPAC issuance for a single year.

- There were numerous notable and successful SPAC acquisitions including DraftKings, Nikola and Open Lending.

- The average IPO performance for Q2 (ex-SPACs) was 40% on day-1 and 58% from offer to June 30.

Mizuho Highlights

- Mizuho served as a Bookrunner or Co-Manager on 27 equity offerings in Q2 which raised $37.5 billion.

- Mizuho was a Bookrunner on 12 of the 27 transactions.

- Notable deals included:

- Active Bookrunner on the $17.9 billion monetization by Softbank of its stake in T-Mobile.

- Active Bookrunner on Norwegian Cruise Line’s concurrent $460 million follow-on and $863 million convertible offering.

- Mizuho currently has 21 bookrun mandates which expect to raise proceeds of ~$10 billion.

TMT Specific Commentary

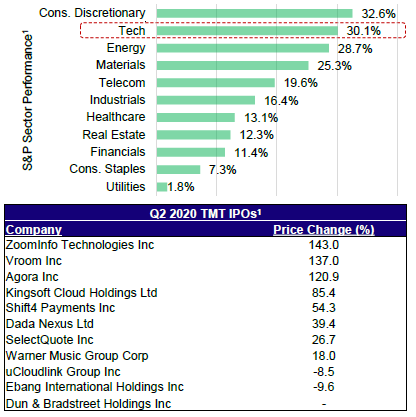

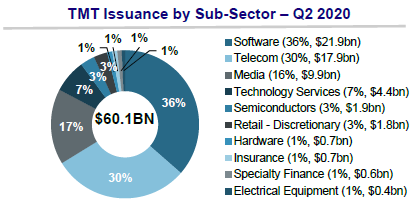

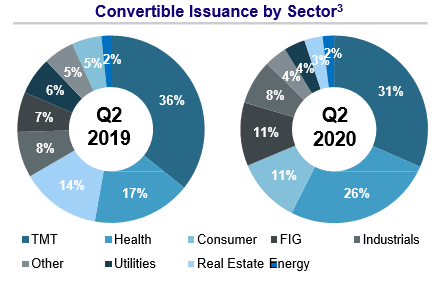

- In Q2 TMT issuers raised a staggering $60 billion - seven and half times Q1’s total of $8 billion - accounting for 32% of total issuance across all sectors.

- “Doom and Gloom” turned into “Zoom and Vroom.” Valuations charged ahead after their Q1 dip. ZoomInfo and Vroom turned in stunning first-day IPO performances as they traded up 62% and 118%, respectively.

- Software represented 36% of TMT issuance in Q2 with $21.9 billion raised.

- Three of the four largest IPOs in Q2 were in the TMT sector: Warner Music ($2.2 billion), Dun & Bradstreet ($2.0 billion) and ZoomInfo ($1.1 billion).

Convertible Market Commentary

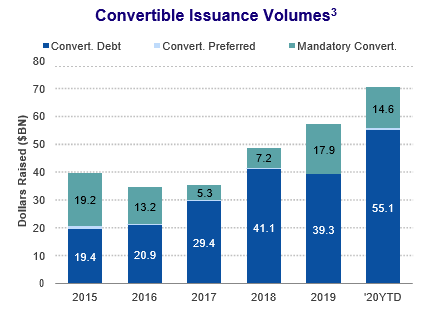

- As of the end of Q2, 114 convertibles had priced to raise an unprecedented $70.4 billion. This exceeded the total for all of 2019 by ~23% and put the convertible new issue market on track to surpass its all-time high of $97.5 billion raised in 2007.

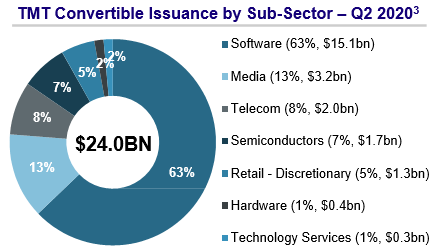

- Terms remained extremely attractive: There were 35 convertibles issued in Q2 by TMT companies to raise ~$24 billion. Median terms were 1.25% coupon, up 32.5% on a 5- year note.

- Eight issuers raised over $1 billion with 6/8 pricing with coupons at 0.625% or lower and conversion premiums at 32.5% or better.

- Software dominated issuance as Palo Alto Networks ($2.00 billion), Coupa ($1.38 billion), Splunk ($1.27 billion), Zscaler ($1.15 billion), Zendesk ($1.15 billion) and Okta ($1.15 billion) all tapped the convertible market.

- The use of derivative structures to increase the conversion premium to either 75% or 100% remained popular as over ~60% of issuers utilized such a structure.

Themes and Thoughts

- COVID-19: As is obvious, WFH did not hinder equity issuance nor a rebound in the stock market. As the northeast seemed to successfully slow the spread, new hotspots in AZ, FL, TX and CA have emerged re-igniting the debate around a second wave of “stay-at-home” orders and shutdowns. This raises new concerns about the strength and resilience of the economic recovery.

- The Election: Four months is an eternity in politics, but with current polls pointing to a Biden victory in November, Wall Street has begun preparing itself for such an outcome. Naturally, the focus is on the likelihood of higher personal/corporate taxes and the implications these policy changes would have on growth.

- Private equity: The presence of private equity firms in the equity capital markets was apparent in Q2 as they backed nine deals raising ~$9 billion, the highest level of proceeds in four years.

- SPACs: Blank-check companies represented 40% (by # of deals) and 33% (by $ volume) of all IPOs YTD through June 30. The status of the product continues to elevate as the IPO market remains muted for issuers outside of the healthcare and TMT sectors. As noted, there were significant successful SPAC mergers in Q2, including VectoIQ/Nikola, Diamond Eagle/DraftKings and Nebula/Open Lending. We expect the use of SPACs to continue to serve as an alternative way for companies to go public for the foreseeable future.

Source: Dealogic, Bloomberg

1: Performance as of 6/30/20; excludes SPACs

2: File to offer discount

3: By dollars raised as of 6/30/20