Commercial Cards as a cash management tool – who would have thought?

Commercial card programs have quickly become an integral part of the global corporate payments ecosystem. Over 10% of global payments are processed through the Commercial Card processing system today, and we expect to see significant further growth as corporate clients better understand how commercial card functionality can be integrated into a payments strategy to help increase efficiency and optimize working capital.

Really? I only use my corporate card to settle T&E and other minor expenses

Commercial card programs for T&E and Purchasing have been around since the early 1990s. Well known to corporate, government, and not-for-profit organizations, they are highly desirable for their ease of use, operational controls, and detailed transaction data in helping organizations better manage their T&E and procurement expenses. Recent upgrades to the card authorization, clearing and settlement infrastructure has allowed banks and their corporate clients to develop exciting new card applications.

Commercial cards go contemporary: ePayables deliver value across the payments ecosystem to corporate clients.

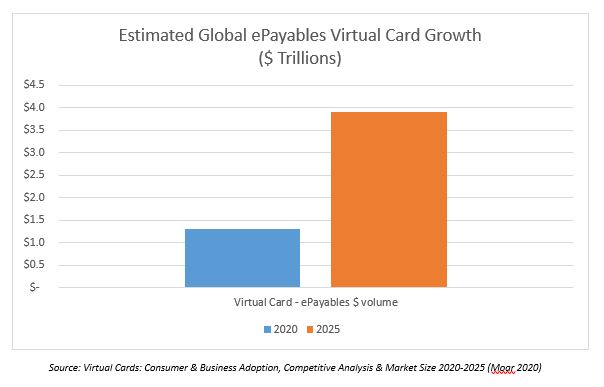

Virtual cards, also known as ePayables, are quickly becoming an alternative to checks and ACH in the accounts payables process. For those organizations that struggled with a lack of access to online banking systems, or even the modest checkbook during the initial months of the 2020/2021 pandemic, virtual cards became a simple alternative to keep the supply chain functioning. Virtual cards are digitally generated commercial cards that do not require the issuance of a plastic card and can be configured for single-use or dedicated to a particular supplier, even funded only for a particular payment, making them extremely safe and secure. Use of these card rails for post invoice B-to-B payments is expected to triple over the next 5 years, from an estimated $1.3 trillion in 2020 to an estimated $3.9 trillion in 2025, according Juniper Research.

Can I really use a card instead of a check? Are there any adoption challenges?

Broad adoption by suppliers is always a challenge to even more robust Virtual Card/ePayables growth, as there is work to be done to ensure they understand the value of these type of payments. Reinforcing important benefits, such as greater process efficiencies, improved working capital management through reduced Days Sales Outstanding, and the delivery of guaranteed funds, will strengthen supplier relationships and lead to adoption success.

The value of Virtual Card payments in the post pandemic environment across the ecosystem include:

Benefits to organizations (Payers)

- Increases Days Payments Outstanding (DPO) - extends payment terms (up to 55 days depending on date of transaction, cycle date and payment date)

- Improves data quality and data visibility – enhances efficiency in the remote work environment

- Optimizes Procurement Negotiations – delivers consolidated enterprise wide data in numerous formats to aid in critical business negotiations

- Delivers Favorable Economics – potential revenue sharing transitions accounts payable payments from a cost center to a revenue generator

- Reduces reliance on issuing checks, often mitigating the risk of fraud

Benefits to suppliers/merchants/vendors

- Reduces Days Outstanding (DSO) – payments generally received within 1 to 2 days

- Guaranteed funds – significantly reduces NSF occurrences

- Improves cash flow – improves the order to cash cycle time

- Enhances accuracy – reduces posting errors

- Reduces reliance on Lockbox and Remote Deposit Capture to deposit paper checks, often mitigating the risk of fraud

Some suppliers object. How do I overcome this?

A good banking partner will guide you through and help you overcome any supplier acceptance challenges for post-invoice, business-to-business accounts payable type payments. While not all suppliers can be convinced to switch from checks and ACH to Virtual Card/ePayables, a significant number will.

But don’t acceptance costs outweigh the benefits?

This can be addressed by a simple business case highlighting the efficiencies of card acceptance and how they reduce both “hard” direct costs and soft “indirect” costs particularly when providing trade terms.

Common costs incurred by suppliers when providing trade terms:

- Credit Risk

- Check Processing

- Delayed Payments

- NSF Fees

Clearly, providing trade terms can be an expensive business.

- Commercial Cards deliver favorable cost benefits to Suppliers from:

- Faster payment receipts

- Reduced card processing costs when invoice-level data is provided

- Enhanced security and efficiency with the electronic tokenization of payment details which delivers payment information securely, more efficiently, and is in a manner much less prone to posting errors.

Partners make the difference: Mizuho can help!

Corporate clients have increasingly complex needs, particularly as the economy begins to recover from the current pandemic. Maximizing payables efficiency is a key area of focus. Clients look to banks and other financial institutions to help improve internal cash flow management practices through payments optimization and access to capital to propel future growth. Mizuho’s Commercial Card service is managed within the organization’s treasury management group and is a valuable component of Mizuho’s overall Cash Management solutions suite. Our Commercial Card service offering delivers a very competitive Virtual Card offering to help solve the needs of our treasury management clients.

Our competitive point of differentiation is embodied in the platform capabilities, supplier enablement expertise, degree of flexibility and level of individual service we deliver that aligns with the needs of our clients – and provides the payments optimization client’s demand in today’s post pandemic world.

This announcement appears as a matter of record only and does not constitute an offer to sell or the solicitation of an offer to buy the securities. Mizuho Americas encompasses several entities and is part of the global Mizuho Financial Group, Inc. Lending, derivatives, and other commercial banking activities are provided in the Americas by Mizuho Bank, Ltd. and its subsidiaries, including Mizuho Bank (USA). Securities, strategic advisory, and other investment banking services are provided in the Americas by Mizuho Securities USA Inc., which is a U.S. SEC registered broker-dealer and a member of FINRA and SIPC. This advertisement is not intended for businesses located in regions outside the Americas © 2021 Mizuho Financial Group, Inc. All rights reserved.

For further information regarding Mizuho U.S. operations, including important disclaimers, please see https://www.mizuhogroup.com/americas/disclosures.

.avif)