Despite advances in technology and best efforts of participants in the financial system, the payment process can still break down.

This means payments may not be made on time, funds may not be deposited to accounts, and information regarding payments may be hard to come by.

Individuals and corporations should always ensure they have plans in place to guarantee they can make payments in a timely manner through business continuity planning (BCP).

BCP enables the continuation of a minimum level of essential services during, and after, the suspension of operations due to:

• natural disasters

• terrorist attacks

• computer or internet issues

• major global events, such as a pandemic.

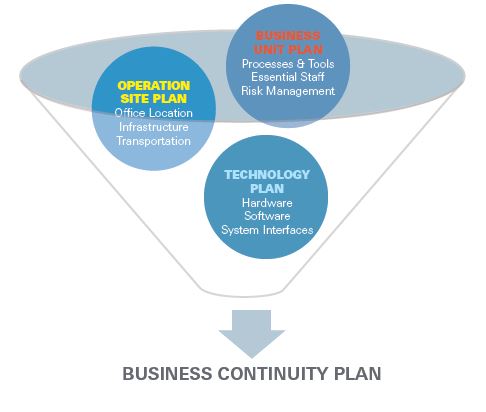

The broad components of BCP are highlighted in the following illustration.

What should BCPs cover?

BCP can take many forms depending on the sophistication of the entity and the type of process failure faced.

Because all firms have their own unique characteristics, it’s important for each to design its own strategy – addressing its particular risk profile – and to review it on an ongoing basis.

For example, many firms found they lacked satisfactory BCP when adapting to the new work-fromhome environment brought about by the global coronavirus pandemic. Almost one year into an essential and extensive work-from-home situation and only recently are many employers finding their way toward an adequate remote working setup for employees.

There have been many lessons for organizations.

Some employees have only a single “family” computer from which to log on to their remote or virtual workstation. Similarly, not all employees have dedicated private spaces to retreat to when joining phone and video conferences, making background noise inevitable. Many employees found they were competing with children in a virtual schooling environment. How can parents prioritize in situations such as this? What should an employer do when an employee’s power or internet service is disrupted? Should employers provide employees hardware and internet?

It is nearly impossible to imagine every scenario for which an individual, corporate, payment service provider, or clearing system should prepare. But at minimum, a BCP should:

1. Ensure customers have access to funds for essential purchases and information to make critical

decisions

2. Prevent possible defaults on payments linked throughout society, with funds received as a counter

value in a first transaction used to pay for another

3. Limit payment and settlement disorder since financial institution operations are deeply intertwined

with broader economic activity

4. Maintain the institution’s and system’s reputation amongst users by exerting strong leadership

which is deeply involved in the process, investing managerial resources, and showing a firm-wide

awareness

5. Enable employees to get payments made in a timely manner in non-traditional work spaces

What to consider when creating a BCP?

When evaluating the preparedness of organizations – particularly payment service providers and clearing systems – important items to consider are:

• planning, testing, and reviewing procedures

• a focus on critical operations

• co-ordination with external parties, as necessary

• consideration of special circumstances for major disruptions

One way to maintain a strong BCP is to prepare an offsite location as a designated contingency payment processing site. These sites can be categorized as:

• ‘hot’ – generally well-staffed, frequently backed-up, and can be activated in a very short amount of time

• ‘warm’ – lightly staffed, with system configuration and back-up download required prior to activation

• ‘cold’ – no staff or regularly backed-up data, reserved for when other locations become inaccessible

• ‘dual-processing’ centres – maintained simultaneously to primary location with mirrored data for seamless integration

At a minimum, the back-up site or dual-payment processing site should be located on a different power grid to the primary site, and, preferably, have in-house generators capable of supplying power for several days.

All BCP should consider which employees are needed to manage these processing sites and which employees can be enabled to work entirely offsite, at home.

Operating under a BCP

Let’s look at some examples individuals, corporations and financial institutions may face when operating under BCP.

In one scenario, ABC Company has received checks from customers, but the electronic system they normally use via a PC, Remote Deposit Capture (RDC), is out of service.

Local bank branches are closed to the public, making a physical deposit unavailable, so how can the Company pay checks into its account?

One option is for ABC Co. to use a mobile app to make the deposit, if available. However, the depositor may need to scan each check individually, and there may be a daily value limit.

If the user has a high volume and value of checks to deposit, using a mobile app may not be a workable option. As an alternative, a bank may allow overnighting checks to its operations site for manual deposit. However, users may not want to bear the cost of this delivery method, since they are ultimately dealing with an interface issue. Should the bank be prepared to absorb these additional costs as a part of its BCP?

In another scenario, a customer needs to pay its vendors, but the e-banking platform used to prepare wire transfers is currently down. Without this interface, the payment service provider may allow emailing or faxing payment instructions to its operations team directly.

However, manual wire transfers will require wet-ink authorized signatures, and may require a call-back by phone to confirm the validity of the instructions.

However, manual wire transfers will require wet-ink authorized signatures, and may require a call-back by phone to confirm the validity of the instructions.

This may not be an issue for an individual but could prove difficult for a corporation with signatories located across various time zones, and a potentially high volume of payments to be made.

Should companies anticipate scenarios like this when determining essential staff, and signatories, for BCPs?

How BCP can adapt to the “new normal”

Many firms over the past year have found that they were unprepared for many aspects of operating during a lengthy period of remote working. Many lessons have been learned and no two firms seem to have approached the problem in the same manner.

Firms who had previously not encouraged employees to work from home, needed to procure some sort of remote access software.

Some, who may have already implemented such systems, elected to provide a stipend to employees who needed additional hardware to maintain a workstation equal to what they were accustomed.

When dealing with the challenges of no longer having access for face-to-face meetings, firms must choose between widely available meeting interfaces such as Google Meetup and Microsoft Teams, or, contract with a vendor like Webex or Adobe to provide dedicated spaces.

It can all work, if there is a well thought out plan.

Test your BCP

We could provide countless examples of scenarios in which robust business continuity plans are needed.

Considering as many situations as possible is key to creating a robust plan that works in the worst of circumstances. In times of uncertainty, even the best laid plans can go awry.

When trying to plan for what you cannot foresee, the best option is to constantly test the system, review the results, and repeat. Flexibility and communication are key.

For further information regarding Mizuho U.S. operations, including important disclaimers, please see https://www.mizuhogroup.com/americas/disclosures.