Overall Equity Capital Markets Commentary

- Thus far in 2022, equity markets have been quite turbulent based on a multitude of macro factors ranging from ongoing inflationary pressures to geopolitical tensions in Eastern Europe. This global economic backdrop caused volatility to spike to its highest levels since October of 2020, which led to a significant decrease in equity issuance across all sectors. At the same time, the Fed increased interest rates by 25bps for the first time since 2018, which is expected to be followed by another five or six rate hikes this year as well as a tapering of its asset purchase program. Going forward, investors will be focused on how the Fed balances inflationary pressures (at a 40-year high) and economic growth at a time of instability in the financial markets.

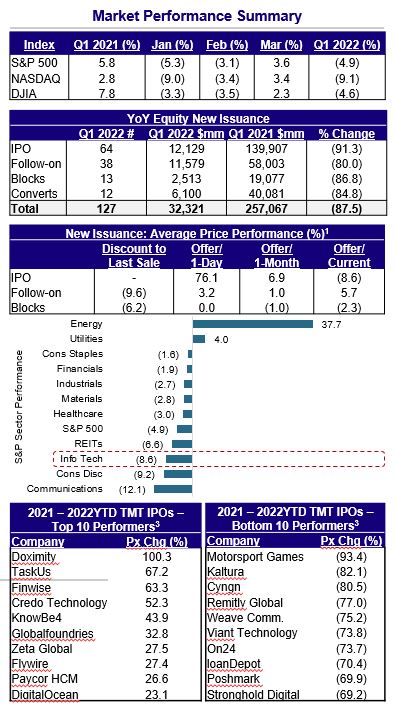

- After another record year in the new issuance market, Q1 2022 experienced a significant decrease in deal activity as IPO proceeds were down ~91%, and secondary proceeds were down ~83% from a year earlier. At one point, no IPOs were priced for 48 days, which was the longest drought since 2011. At that point in time, the European debt crisis was unfolding, S&P had just downgraded the US, and the VIX was at a post-crisis high.

- Over $30bn of equity issuance took place in Q1 2022, of which only ~$2.1bn, or ~7% of total issuance, were traditional IPOs. There was only one IPO (TPG Inc.) that raised more than $1bn in proceeds. This was a stark difference compared to Q1 2021, which saw ten $1bn+ IPOs. Although a small sample size, 2022 traditional IPOs have performed better than the Class of 2021 as their average and median return was ~(8.6)% and ~(6.0)%, respectively, relative to 2021 IPO’s average and median return of ~(30.9)% and ~(39.8)%, respectively.

- The SPAC IPO market remained open, albeit with terms that were more investor friendly than a year ago. The SPAC market saw 54 SPACs raise ~$9.9bn in proceeds in Q1 2022. Proceeds were down ~90% from a year earlier, but represented ~84% by number of deals and ~82% by proceeds raised, respectively, of the IPO market in Q1 2022. In addition, there were 29 successful business combinations worth over $44bn.

TMT Specific Commentary

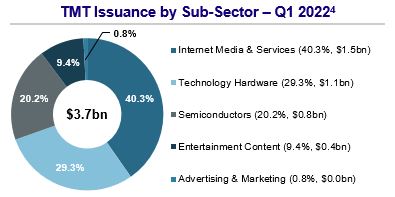

- In Q1 2022, TMT issuers raised ~$3.7bn, which amounted to ~7% of TMT’s Q1 2021 proceeds and ~12% of total issuance in Q1 2022.

- Credo Technology was the only TMT IPO that priced during the quarter. The semiconductor company posted an impressive ~52.3% return. Demand was underpinned by cornerstone investors indicating an interest to purchase up to an aggregate of $120mm in ordinary shares at IPO. Mizuho served as a Bookrunner on the IPO.

- The Internet Media & Services sector generated the most proceeds in the TMT space, but this was generated from only one deal – SNAP’s $1.5bn Convert.

- Similar to last year, 2021 TMT IPOs continue to trade well below their IPO price. At one point during the quarter, it was noted that 1/3rd were trading below their last funding round levels. Notable underperformers included Motorsport Games ~(93.4)%, Waterdrop ~(87.7)%, Robinhood ~(64.4)%, and UiPath ~(61.4)%.

- During this time of economic uncertainty, valuations in the TMT space have been drastically affected as high growth company multiples have fallen to pre-Covid levels.

Convertible Market Commentary

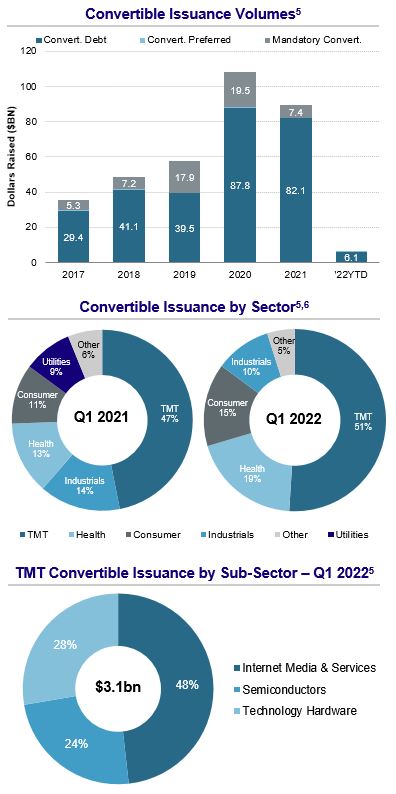

- Convertible issuance in 2022 has been relatively muted as only 12 converts priced in Q1 2022, generating ~$6.1bn in proceeds. This is only ~17% of total deals and ~15% of proceeds raised in Q1 2021. TMT accounted for 25% of convert deals priced as well as ~51% of proceeds raised.

- Terms remained extremely attractive: 3 TMT issuers raised convertible proceeds at average terms of ~0.25% coupon and up ~40% on a ~6 year note. The use of the call-spread was nonexistent as no TMT issuers utilized the structure.

- In the 2021 TMT Year in Review, we noted “a rising interest rate environment should continue to make the convertible market an attractive product for issuers.” Although issuance has not been as abundant as some would think, we still believe the product is a strong alternative to selling common equity.

Themes and Thoughts

- Russia and Ukraine Conflict – On February 24th, Russia launched a full-scale military invasion into Ukraine. Not only have these actions resulted in thousands of civilian deaths and pushed millions of Ukrainians to neighboring countries, but the world economy has also felt the ripple effects. Commodity prices have surged to all-time highs as crude oil topped $130 for the first time since 2008. These increases in prices have only added more pressure on the Fed and other key central banks around the world to tighten monetary policy. With no end in sight, it will be interesting to see how investors position themselves during the ongoing conflict.

- Expected Rate Hikes and Fed Tapering – With already one interest rate hike in 2022, many expect the Fed to continue with this hawkish sentiment throughout the year and even into 2023. Fed chair Jerome Powell reiterated his hawkish tone in a speech on March 21st as he stated nothing was preventing a 50bp rate increase at their next meeting in May. He further noted that high inflation only underscored the need to move expeditiously. This coincides with their plan to shrink the Fed balance sheet, which could also come as soon as their next meeting in May and likely push long term borrowing costs higher.

- Increased Volatility – Due to ongoing geopolitical tensions and uncertainty with the Fed, the VIX, often known as Wall Street’s fear gauge, has significantly spiked in 2022. This had led to a lack of stability in the index, resulting in a slowdown in the issuance market that is expected to continue as companies navigate the ambiguity in the market.

Mizuho Highlights

In Q1 2022, Mizuho ECM participated in 9 equity deals generating ~$5.5bn in proceeds, of which 7 were bookrun deals amounting to ~$4.1bn in proceeds.

- Mizuho was an underwriter on 2 of the 10 Regular Way IPOs during the quarter, which accounted for ~58% of the total IPO proceeds raised.

- As noted, Mizuho was a bookrunner on the only TMT IPO in Q1 2022 – Credo Technology, which raised $230mm in late January.

Source: Dealogic, Bloomberg

1. Performance metrics are for all U.S. listed IPOs in 2022YTD excluding SPACs; Deal size > $25mm

2. S&P sector performance from 12/31/21 to 03/31/22

3. Top/Bottom performers include U.S. companies only

4. Deal size > $25mm

5. Calculated off dollars raised; Deal Size > $25mm

6. “Other” includes: Real Estate, FIG, & Energy