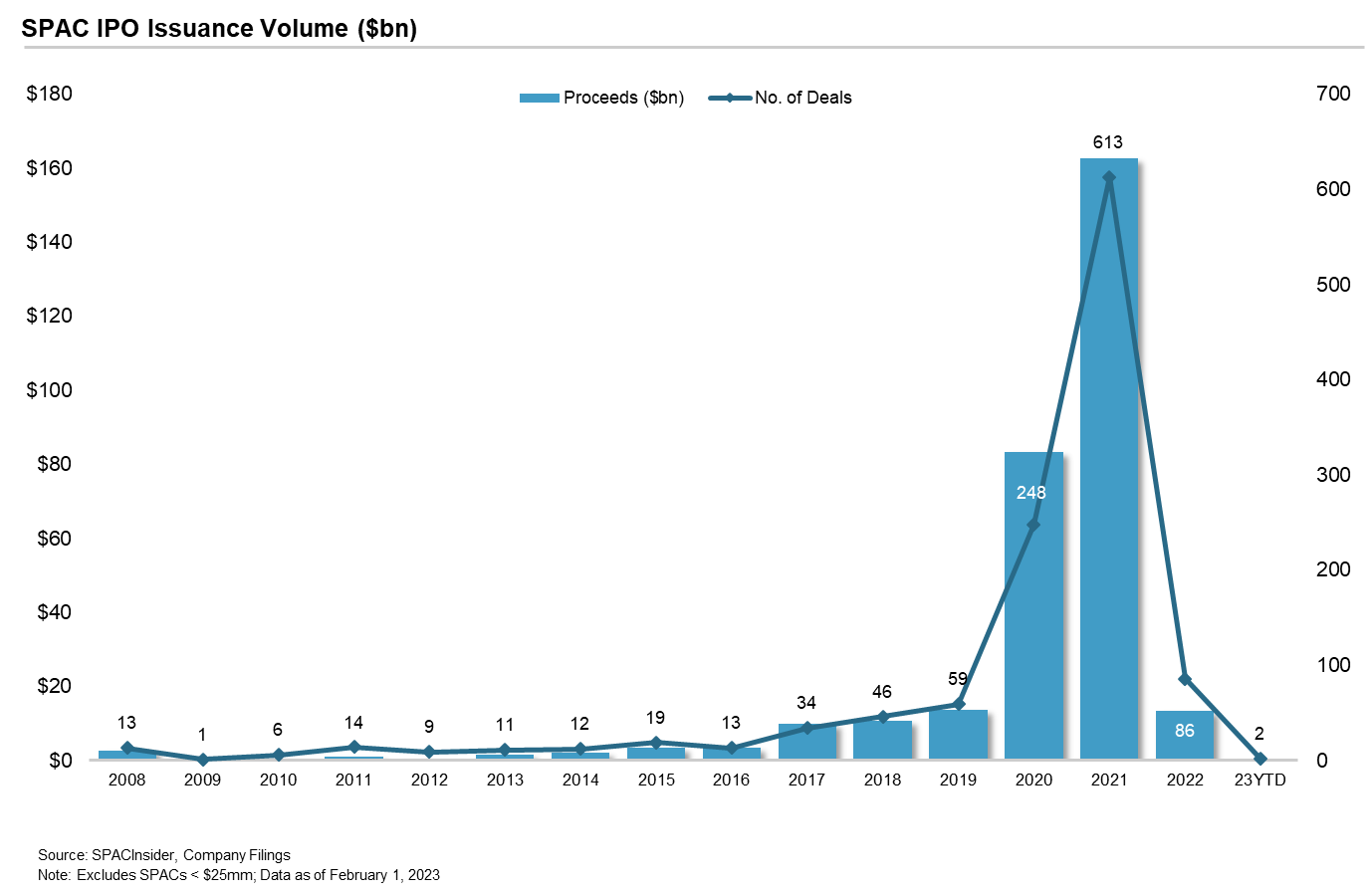

When Q1 2021 wrapped up, the quarter saw some 300 SPACs raise $100 billion. That was an extraordinary feat. It seemed that literally everyone you knew was doing a SPAC. SPACs, short for Special Purpose Acquisition Companies (also known as blank check companies), occupied cocktail party conversations, club house conversations and water cooler conversations. Celebrities, private equity firms, and hedge funds were backing SPACs. And, bankers were happy to join the SPAC party given the opportunity to earn underwriting fees, M&A advisory fees and the associated league table credit.

The SPAC Boom

But, did anyone really think that this pace of issuance would continue? Let’s extrapolate: $400 billion of SPAC issuance and 1,200 SPACs in a calendar year? Not a chance. For the twelve years from 2008 until 2019 (the year before things started going ballistic), there were a total of 237 SPACs that raised $50 billion. So, in the first three months of 2021, SPACs raised twice the amount of capital raised in that twelve year period. If you include 2020, which saw 248 SPACs raise $83 billion, the entire “modern era” of SPACs prior to 2021 represented $133 billion over 485 deals. People often say Wall Street is famous for beating a product into submission. 2021 was that year for SPACs. For the year, SPACs raised $162 billion across 613 deals. Yet, SPACs are meant to be just one of several routes to the public markets – among them, the traditional IPO, the Direct Listing (only 13 in the last 5 years) and the SPAC. The “traditional IPO” (non-SPAC, non-Direct Listing) market is about a $100+ billion a year market and represents about 200-300 companies going public. If the “SPAC option” is supposed to be a subset of the overall IPO market, you can see the problem. In 2021, SPACs raised more than 1.5X the average annual IPO market! There simply are/were not enough public worthy companies to satisfy all of these SPACs.

The Turning of Tides

As CNBC touted the “alternate IPO” featuring various SPAC evangelists, the more cynical folks started to look away for fear of witnessing the inevitable train wreck that was on the horizon. You see, SPACs were always designed for entrepreneurs and proven operators to identify private companies that were on the cusp of IPO-readiness. These companies would benefit from the skill and experience of the SPAC team to help them improve, grow and succeed in a public framework. Core to a successful SPAC team was unique access to deal flow. Like an IPO, one of the key attributes of a SPAC merger is acquiring the asset at an appropriate discount to the public comparables (i.e., an “IPO discount”). The moment hundreds of SPACs were competing for limited assets, the dynamic changed to an auction format – the “SPAC-off” – where multiple SPACs were invited to bid in a sell-side process. This destroyed the traditional SPAC process and led to inflated valuations and angst amongst SPAC issuers running against the SPAC clock. It also made it much more challenging to secure long-only investors at the time of the business combination given the poor trading performance due to the stretched valuations being paid (only to be further exacerbated by the market slide in 2022).

The Onset of a SPAC Winter

On April 12, 2021 (12 days after the record Q1 2021 issuance), the SEC fired a shot across the bow of the fleet of SPAC issuance announcing that the accounting treatment of warrants should likely be as a “liability” rather than as “equity” (warrants were a component of the original unit sold at the time of the SPAC IPO and behave like a call option potentially adding incremental value to the investor should the stock price rise materially after the business combination). In the blink of an eye, issuance ground to a halt and panic set in amongst existing and pending SPACs as the vast majority likely had to restate their financials. However, with due credit to the legal and accounting community, changes were made to the warrant structure which enabled them to regain their classification as “equity.” One pothole averted and issuance resumed. By the time Q1 2022 was drawing to a close, there were over 600 SPACs representing over $160 billion in search of acquisitions. This was essentially the peak by number of SPACs searching and SPAC capital outstanding. On March 30, 2022 the SEC fired another shot – but this time, an arrow right at the heart of the SPAC market. In the newly proposed rules (which the SEC states is a “clarification” of existing rules) the SEC mandated:

• New disclosure requirements regarding the sponsor economics, potential conflicts of interest and dilution to shareholders;

• The need for Fairness Opinions under certain circumstances;

• Aligning de-SPACs with traditional IPOs – this includes making the private company a co-registrant, eliminating any safe harbor protection for forward looking statements, deeming any SPAC IPO underwriter to be an “underwriter” of the de-SPAC transaction;

• Additional directives on disclosure, use of projections, etc.

This SEC announcement effectively froze the SPAC market. Underwriters frantically tried to figure out what this meant for their de-SPAC M&A business. It is one thing to underwrite a blind pool SPAC led by respected executives for whom background checks and references have been scrutinized. It is another thing to take on prospectus liability for a non-revenue or money losing EV manufacturer or biotech company valuing itself based on 2026 projections. Almost immediately, many banks announced they were no longer willing to advise on SPAC mergers and new issuance all but stopped.

On August 16, 2022 President Biden signed into law the Inflation Reduction Act. Buried within this Act was a 1% excise tax on share buybacks initiated after January 1, 2023 by public companies. Whether accidental or purposeful, the reading of this portion of the Act seemed to capture SPAC liquidations and redemptions. A new panic washed through the SPAC market as it was very unclear who would bear the burden of this excise tax: the trust account or the SPAC sponsors directly? For SPACs that were due to mature in Q1 2023 (remember the 300 SPACs that raised $100 billion in Q1 2021?), many threw in the towel and put the wheels in motion to liquidate early (prior to December 31, 2022). From September 1, 2022 until December 31, 2022, 126 SPACs liquidated representing $40 billion. In December alone, the amount was 91 SPACs for $30 billion. All told for the four months, this was pushing 30% of all outstanding SPACs by both number and capital. What makes this both sad and comical is that on December 27th, while almost all were working off their holiday meals and preparing their New Year’s celebrations, the US Treasury issued guidance that the 1% excise tax doesn’t apply to SPAC liquidations. Unfortunately, this was a little late for those that had now prematurely terminated their SPACs.

A Case for the Comeback

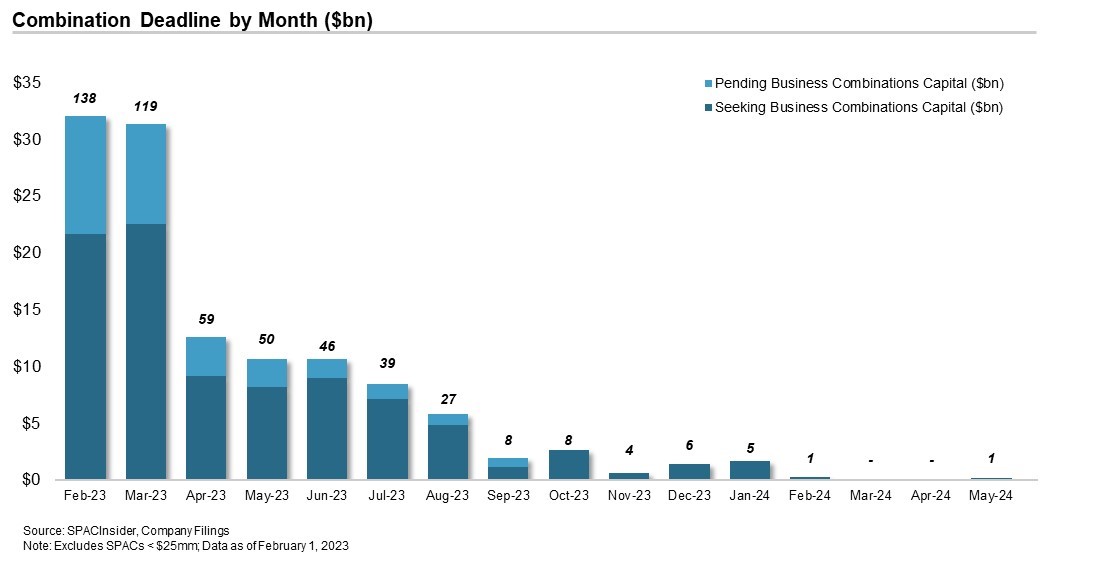

So, that brings us to today. As of today, there are over 350 SPACs representing $91 billion that are actively seeking an acquisition (there are also 155 SPACS representing $30 billion that have announced a business combination). Of the 350+ SPACs, roughly 44% (156 SPACs worth $44 billion) are set to expire by March 31, 2023. Of those that have announced a business combination, 101 SPACs with $20 billion have a March 31, 2023 deadline. So, you have a total of almost 260 SPACs with just shy of $65 billion that have a deadline within 60 days. Said differently, almost 55% of all outstanding SPAC capital reaches maturity by March 31, 2023 (barring any extensions). This will leave about $50 billion outstanding. By June 30, 2023 another $34 billion of SPACs are set to mature. In the absence of new issuance, outstanding SPAC capital will drop to approximately $23 billion. From peak to trough (about 15 months) almost $140 billion will have been returned to SPAC investors! Where will this money go??

The SPAC Renaissance

I love speaking to SPAC investors – truly. I enjoy the banter around structure, market conditions and management teams. But, I challenge when they say they don’t need to invest in SPACs and can reallocate all this returned capital to other strategies – and we know they’re not sending it back to their LPs. Investors want (need!) a reasonably sized SPAC market and therein lies the renaissance. For the first time in 3+ years, there will be scarcity in the SPAC market. This should create opportunity for the bold – admittedly, it is not easy to venture in to the SPAC waters where there still remains some regulatory uncertainty (for issuers and banks), a questionable reputation and potentially reluctance from private companies to engage. But, if you like to consider odds, they certainly look a lot better in a world where there are only 30-50 SPACs in existence versus 600+ (barring new IPOs, as of now there will only be ~20 SPACS in existence after September 30, 2023). The competition for assets will massively decrease - “SPAC-offs” won’t exist. There will almost certainly be fewer banks engaged in the SPAC market. And, investors will need product. While I don’t see a quick return to the 24 month, $10 in trust, ¼ warrant structure, I do think there will be appetite for 12-18 months, $10+ in trust (interest rates will necessitate overfunding of the trust) and a ~1 warrant structure. Market conditions will dictate timing but it certainly seems that Q2/Q3 of 2023 onwards might be a very interesting time to launch a new SPAC. We at Mizuho remain in the SPAC business and we welcome enquiries from the bold.