Environmental Policies and Targets

Environmental Policy

Mizuho's Approach to Achieving Net Zero by 2050

Net Zero Transition Plan

Mizuho's Net Zero Transition Plan (overview)

1 CCS:Carbon dioxide Capture and Storage

2 SAF:Sustainable Aviation Fuel

Third–Party Verification

Education for our Executive Officers and Employees

Mizuho provides education, training, and information to ensure our executive officers and employees comply with all relevant regulations and processes. We also provide training programs, internal communication tools, and study sessions with related companies and departments to deepen understanding about environmental and human rights issues with the objective of promoting awareness throughout our organization so all executive officers and employees will conduct their duties conscientiously.

Environmental Policy

1. Purpose

Our commitment to environmentally conscious action is included in the Mizuho Code of Conduct. This Environmental Policy stipulates the objectives that form the basis of our conduct and the specific actions we will take to achieve them. This policy has been established by a decision of the President & CEO and applies to all group companies of Mizuho Financial Group, Inc.

2. Our approach to addressing environmental issues

Environmental issues are becoming more diverse and complex, and are recognized as one of the most pressing global concerns.

Our economy, industries and society are supported by the varied benefits received from natural capital1 and ecosystems. We believe that addressing environmental initiatives which impact such resources is humanity's shared responsibility towards a sustainable society.

At Mizuho, we recognize that our business activities may have both a direct and indirect impact upon the environment. We also believe that environmental initiatives such as mitigating and adapting to the impact of climate change, preserving biodiversity, and promoting circular economy are essential preconditions for the existence and activities of our company.

While maintaining a global and long–term perspective of risks and opportunities, we are aiming to enhance our corporate value and contribute to the creation of a sustainable society. We intend to achieve this by proactively implementing environmental initiatives which draw on our capabilities and knowledge of our group.

3. Initiatives facilitated by our business activities

- We leverage our financial intermediary and consulting capabilities in order to proactively develop and offer financial products and services which support the environmental initiatives of corporations and other clients. In doing so, we aim to maximize positive impacts and avoid or mitigate negative impacts on the environment.

- We have established an environmental management policy for business activity (PDF/719KB) which we will revise as needed.

- Mizuho Bank complies with the Equator Principles in regard to project finance deals and the management of environmental and social risk.

- In regard to our asset management operations, Mizuho Trust & Banking and Asset Management One engage in dialogue with companies they invest in regarding ESG–related concerns, monitor the companies they entrust asset management operations to, and take other such actions to appropriately fulfill their stewardship responsibilities2 as responsible institutional investors.

4. Efforts to reduce our environmental impact

- We are working to reduce the environmental impact of our own business activities, including through the use of sustainable energy and resources, pollution prevention and practicing sustainable procurement.

5. Governance and management framework

- Our efforts go beyond merely complying with environmental laws and regulations. We support local and international initiatives which aim to contribute to the creation of a sustainable society. In addition, we promote efforts which are aligned to relevant frameworks in each country and region.

- We incorporate environmental risks and opportunities into our strategy and work to manage them appropriately.

- Mizuho Financial Group has put in place a framework for ensuring steady implementation of initiatives towards realizing a sustainable society. This includes regular reports to the Board of Directors regarding progress on environmental initiatives and other information. We have also set indicators and goals related to our environmental initiatives and seek continuous improvement through regular progress evaluation and revision.

- Our group companies implement environmental initiatives under a governance and management framework aligned with their respective business structure and scale.

- In order to ensure compliance with and full implementation of this Environmental Policy, we will train all executive officers and employees.

- To ensure transparency, we will proactively disclose updates as appropriate on our environmental initiatives.

6. Stakeholder engagement

- Mizuho believes in constructive dialogue with our stakeholders through collaboration and cooperation with diverse stakeholders including customers, suppliers, local communities and government organizations.

7. Addressing specific environmental concerns

- Efforts to address climate change:

- We recognize climate change as one of the most crucial global issues with the potential to impact the stability of financial markets, representing a threat to the environment, society, people's lifestyles and businesses.

- At the same time, we believe there are new business opportunities arising from the need to transition to a low–carbon society, such as the field of renewable energy and other businesses and innovations which contribute to mitigating and adapting to the impact of climate change.

- Mizuho supports the Paris Agreement's objective to “strengthen the global response to the threat of climate change”

- In light of this, we have included responding to climate change as a key pillar of our business strategy and will take the following actions in order to proactively fulfill our role in the effort to achieve a low–carbon society (achieve net zero greenhouse gas emissions) and to develop a climate change resilient society by 2050.

- We are directing finance flows towards achievement of the Paris Agreement targets to limit in the global average temperature rise, and we are undertaking phased transformation to a finance portfolio aligned with said targets.

- We will engage in proactive, constructive dialogue in response to our clients' individual concerns and needs, and in support of their efforts to introduce climate change countermeasures and transition to a low–carbon society in both the medium and long term.

- We will proactively develop and offer financial products and services designed to support clients' efforts to introduce climate change countermeasures and transition to a low–carbon society.

- We understand the importance of climate–related financial disclosures and we utilize the framework under the Recommendations of the TCFD in order to leverage growth opportunities and strengthen risk management as well as disclose information in a transparent manner regarding our progress.

- 1 Natural capital: The world's stock of renewable and non–renewable natural resources (e.g. plants, animals, air, water, land, and metals) which afford humanity all manner of benefits.

- 2 Stewardship responsibilities: The responsibilities of institutional investors to enhance the medium– to long–term investment return for their clients and ultimate beneficiaries by improving and fostering the enterprise value and sustainable growth of investment recipients through constructive engagement, or purposeful dialogue, based on in–depth knowledge of the companies and their respective business environments.

Mizuho's Approach to Achieving Net Zero by 2050

Mizuho's goal

Climate change is one of the most important global issues, and it cannot be addressed unless all countries and all stakeholders make efforts to reach the same targets. It is necessary that responses to climate change be based on the best available science, including the expertise of the Intergovernmental Panel on Climate Change (IPCC).

Mizuho recognizes that the impact of climate change would be much less if the global temperature were to increase by 1.5°C instead of 2°C. We believe that the next ten years will be crucial in terms of limiting the rise in temperature to the 1.5°C target. This is why we are pursuing efforts to limit the temperature increase to this amount. As part of such efforts, Mizuho is aiming to become carbon neutral for Scope 1 and 2 greenhouse gas (GHG) emissions by FY2030, and to reduce Scope 3 GHG emissions produced via our finance portfolio to net zero by 2050.

We recognize that abrupt, disorderly changes can have severe economic and societal impacts. Accordingly, at Mizuho, we are aiming for an orderly, just transition.

Mizuho's steps to achieving net–zero emissions

At Mizuho, we recognize the importance of the role financial institutions play in achieving a net–zero real economy. Financial institutions should support clients' climate change countermeasures and the transition to a low–carbon society. This support should be grounded in an understanding that the transition process will differ by location and industry type. In order for us to fulfil our role as a financial institution, Mizuho conducts engagement with clients and requests that they share their transition strategies. Through this client engagement, we confirm the status of our clients' transition strategies and provide clients with support that facilitates the execution of said strategies. If a client shows no progress towards strategy execution despite multiple efforts to engage them to do so, we carefully consider whether or not to continue our business with them.

The road to net zero will vary by business location and industry type. Strong national leadership with effective policies and the establishment of next–generation technology are essential in speeding up the transition towards net–zero emissions. At present, there is a gap between, on the one hand, current commitments, government policy, and technology, and on the other hand, the road to limiting the global temperature increase to 1.5°C. At Mizuho, we believe we must work together with stakeholders to bridge this gap. Mizuho supports government policy aimed at an orderly transition in the jurisdictions where we operate. We do this through our business activities across regions and economies, industry groups, and initiatives. We also proactively support the development and application of innovative, clean, next–generation technology.

Further, Mizuho is continually enhancing our climate risk management for the purpose of stabilizing financial markets. In these ways, we are contributing to the achievement of a low–carbon society and the development of a climate change–resilient society by 2050.

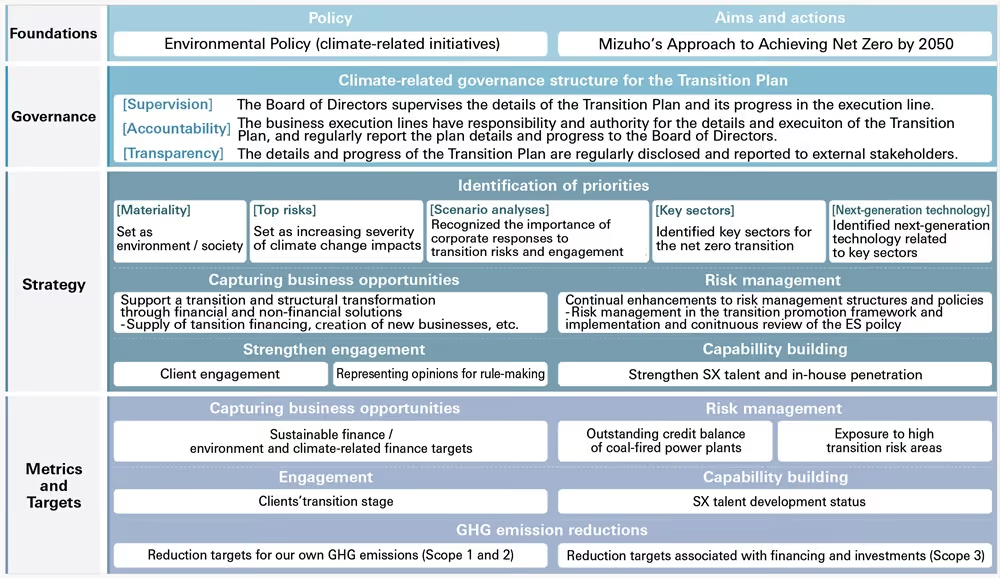

Addressing Climate Change (Initiatives based on TCFD Recommendations)

The TCFD Recommendations call for disclosures on corporate governance, strategy, risk management, and indicators and targets relevant to climate change–related risks and opportunities.

At Mizuho, we have supported the intent and aims of the TCFD Recommendations since December 2017, and we are working to engage in initiatives and enhance disclosures in accordance with the recommendations. The current status of our response to the TCFD Recommendations is as follows.

Climate & Nature-related Report

Governance

- Mizuho has established a supervisory and business execution governance framework, centered on the Board of Directors.

- Supervisory: The Board of Directors and the Risk Committee conduct oversight on reported and deliberated matters.

- Business execution: The Sustainability Promotion Committee, the Risk Management Committee, the Executive Management Committee, and other committees hold deliberations and discussions, which are reported to the Board of Directors.

- The Group Chief Sustainability Officer (CSuO) and the Group Chief Risk Officer (CRO) lead initiatives in their respective areas under the Group CEO's supervision.

- Mizuho has adopted sustainability-related indicators for evaluating executive compensation.

Strategy

- Mizuho has developed the Net Zero Transition Plan (formulated in 2022, revised in 2023) to promote the Group's climate change responses in an integrated manner.

- Recognition of opportunities and initiatives to capture opportunities:

- We recognize transformations in industrial and business structures toward the transition to a decarbonized society and investments in and implementation of practical applications of new technologies as opportunities.

- Based on sustainable business strategies, we actively support clients' transitions to a decarbonized society and their measures to address climate change.

- Support for steady transitions by clients: We promote support for clients' business portfolio restructuring and social implementation of next-generation technologies. We have strengthened our financing capacity toward our sustainable finance target of JPY 100 trillion over the FY2019 to FY2030 period.

- Promotion of future-oriented actions by clients: We have strengthened efforts in the focused areas of hydrogen, carbon credits, and impact, and we have expanded new business domains. We support the establishment of technologies and business models in the development, demonstration, and commercialization stages through the Transition Equity Investment Facility and Value Co-creation Investments.

- Engagement

- To improve the effectiveness of client engagement, Mizuho developed the “Grand Design” and enhanced dialogue using GHG emissions as a starting point.

- We have enhanced our communications with policy makers and our involvement in international rule making, making use of our industrial insight.

- Capability building

- We are shifting from establishing framework and knowledge accumulation to a stage focused on creation of output.

- We promote capability-building initiatives both within and outside Mizuho, such as enhancing stakeholder collaboration and co-creation, raising employee awareness, and consolidating employee capabilities.

- Risk recognition: We comprehensively ascertain the risks associated with climate change by assessing the importance in each risk category.

- We recognize credit risk (deterioration of client business performance) to be of particularly high consequence.

- Scenario analyses and strategy resilience assessments:

Risk management

- As part of the Top Risk Management framework, where top management recognizes risks with significant impacts on Mizuho, worsening impacts of climate change and inadequate environmental responses has been designated as a top risk, and we strengthened control measures.

- Based on the Basic Policy for Climate-related Risk Management, we recognized risks and assessed risks related to materiality. For material risks, we identify and manage quantitative impacts through scenario analysis and credit risk assessments.

- Risk control in carbon-related sectors:

- We have established a risk control framework to assess and monitor the degree of risks for each client along two axes — (1) the client's sector and (2) the status of the client's transition risk responses. (We added GHG emissions reduction performance and alignment of targets and results with the 1.5℃ pathway to axis (2).)

- We control exposure in high-risk areas by promoting transition through engagement and assistance.

- We have established and operate the Environmental and Social Management Policy for Financial Activities*(ES Policy). The following aspects of the ES Policy were revised in February 2025:

- Conduct due diligence when considering financing or investing in regions with high conservation value, and prohibit financing or investing in projects that involve illegal logging (revisions to be implemented in July 2025).

* In 2025, the name was changed from the previous " Environmental and Social Management Policy for Financing and Investment Activity" to " Environmental and Social Management Policy for Financial Activities."

- Conduct due diligence when considering financing or investing in regions with high conservation value, and prohibit financing or investing in projects that involve illegal logging (revisions to be implemented in July 2025).

Metrics and targets

Data for disclosure aside from monitoring metrics:

- Sector-by-sector credit exposure in line with the TCFD Recommendations

- GHG emissions from financing and investment / capital market activities (financed emissions / facilitated emissions)

- Expansion of disclosure metrics

- The scope of Scope 1 and 2 reduction targets has been expanded from seven group companies to include all domestic and international consolidated subsidiaries.

- For oil and gas sector of Scope 3 targets, the targeted value chain has been extended to include gas liquefaction and oil refining, in addition to the initial targets for upstream production (exploration, development, and production).

- The funds used for the construction or expansion of coal-fired power plants, which is prohibited under the ES policy.

- See p.45 "Risk Control in Carbon-related Sectors" (PDF/3,926KB) for the definition of exposure to high-risk areas.